New Report: LATAM's rise in global crypto markets

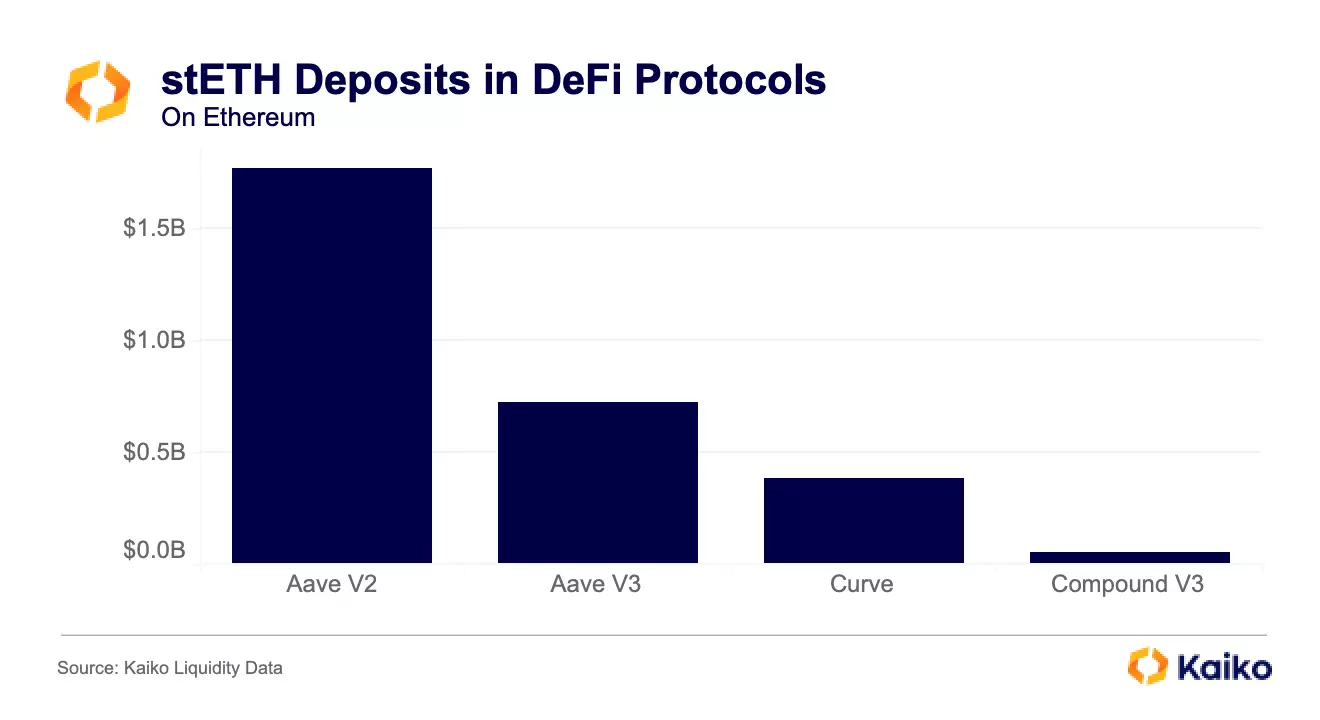

Is stETH Liquid Enough?

Written by Riyad Carey

06/07/2023

Welcome to Deep Dive!

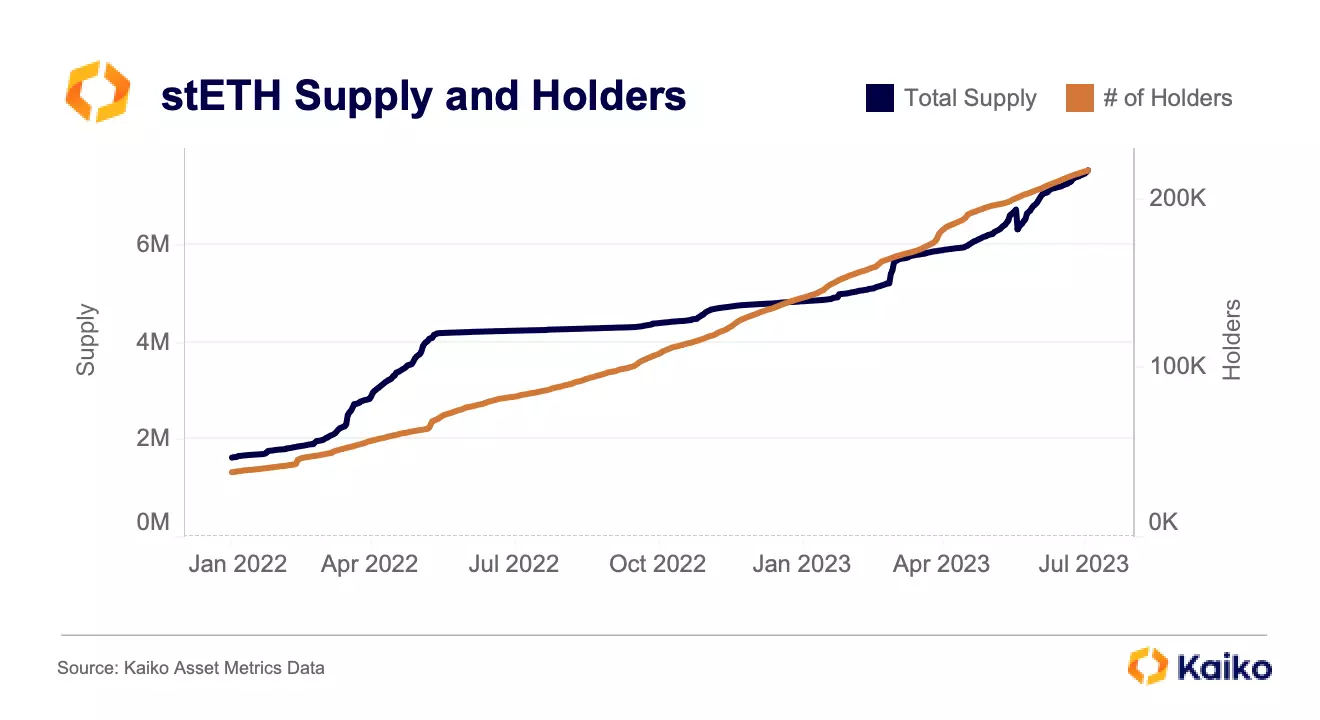

Three Arrows Capital famously blew up because of a series of bad trades, primarily Luna and GBTC. What happened to Luna is obvious: it went to 0 because of UST’s flawed peg maintenance mechanism. The GBTC situation was a bit more complex: “Grayscale allowed big investors like 3AC to purchase shares directly by giving Bitcoin to the trust. These GBTC holders could then sell the shares to the secondary market. That premium meant any sales could net an attractive profit for the big investors.” However, “shares bought directly from Grayscale were locked up for six months at a time. And starting in early 2021, that restriction became a problem. GBTC’s price slipped from a premium into a discount,” which was especially devastating for firms like 3AC, which used leverage to enhance its returns.

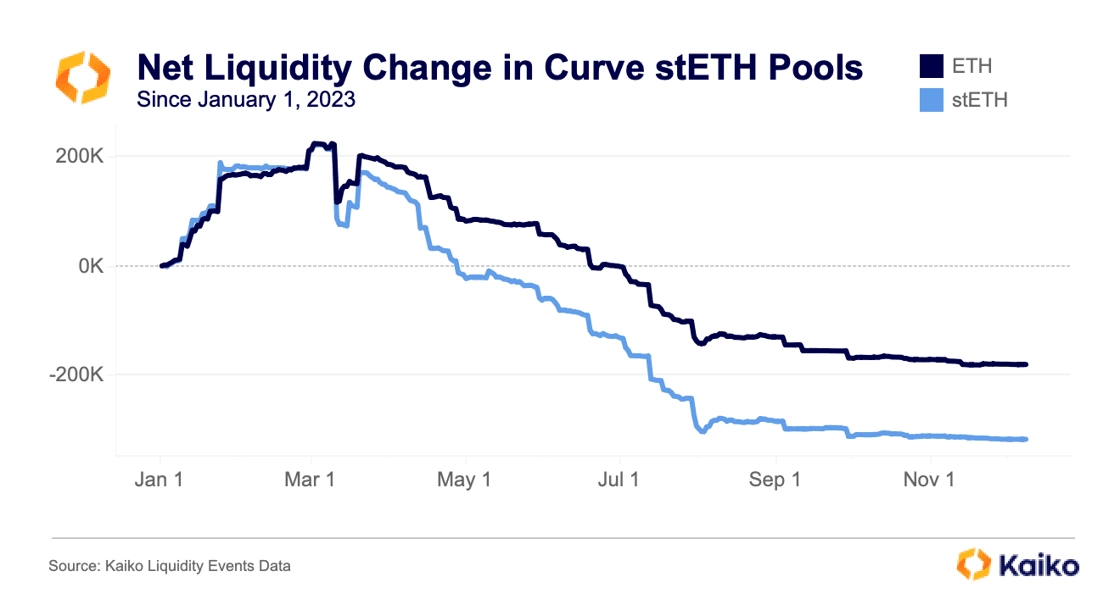

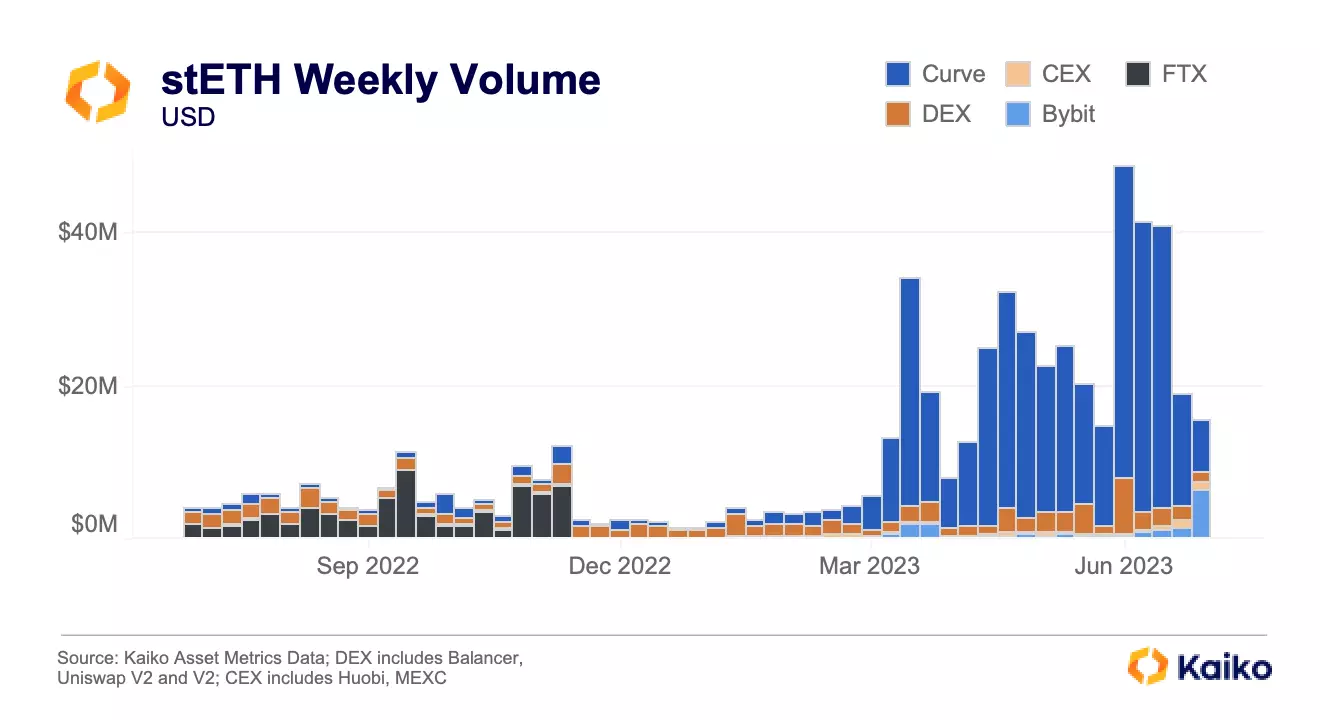

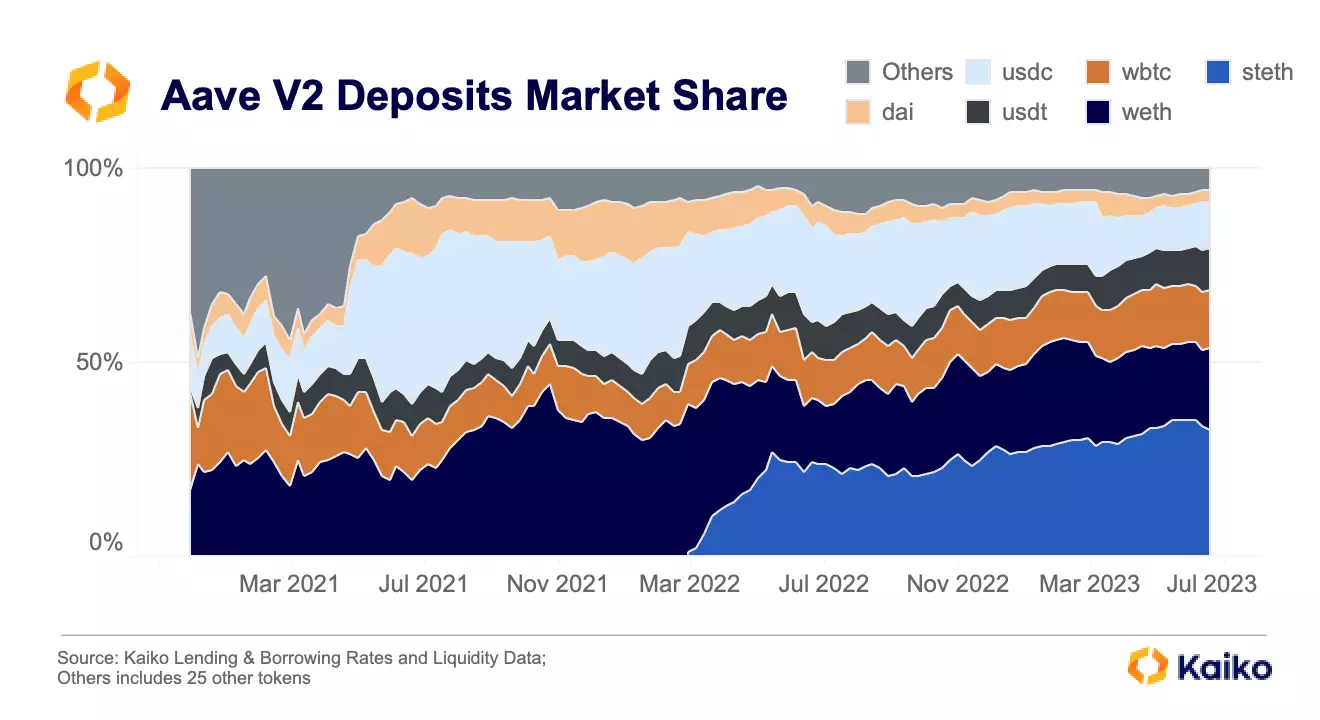

Essentially, 3AC made a bet that GBTC – a fundamentally different asset than BTC, with significant frictions in entrance and exit – would closely track BTC’s price. This saga has been front of mind as I’ve observed stETH (and other liquid staking derivatives) begin to displace ETH in DeFi protocols.

More From Kaiko Research

![]()

Bitcoin

14/07/2025 Data Debrief

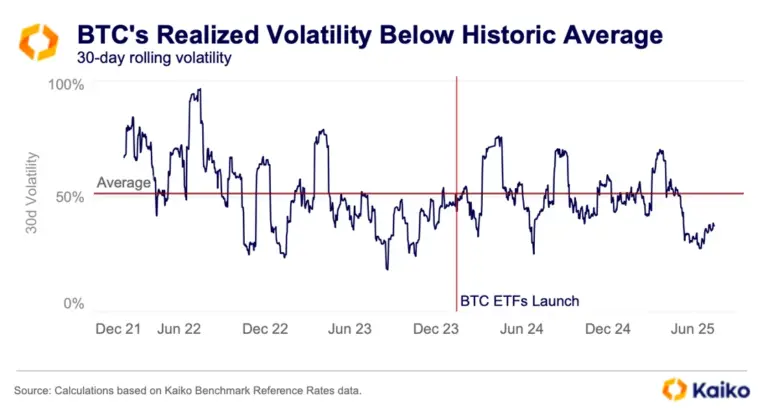

Bitcoin Booms in Low-Risk EnvironmentBitcoin topped $123k for the first time on Monday as last week’s rally extended into a second week. Today we’re going to explore the latest all-time highs in the context of portfolio risk, focusing on how BTC has consistently set highs during low volatility periods in recent months.

Written by The Kaiko Research Team![]()

USDC

07/07/2025 Data Debrief

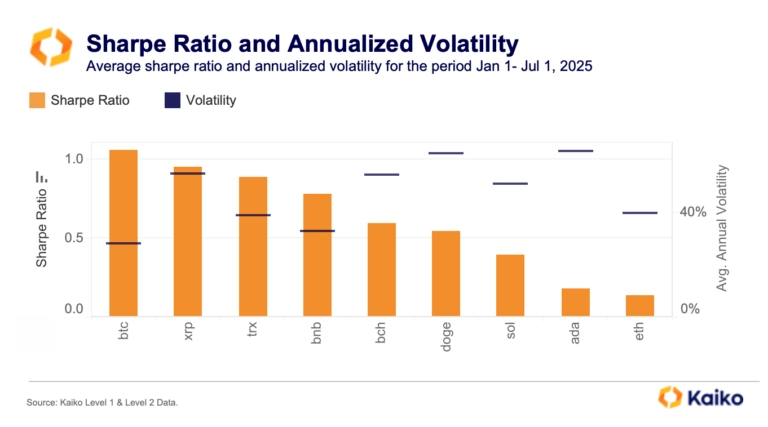

Gap grows between Bitcoin and altcoins.Bitcoin came close to a new all-time high last week before strong U.S. jobs data dented rate-cut hopes and pulled markets lower. Yet momentum remains intact, driven by institutional demand and a clear shift toward Bitcoin over altcoins. This week, we explored the structural shifts that may be laying the groundwork for a breakout.

Written by The Kaiko Research Team![]()

USDC

30/06/2025 Data Debrief

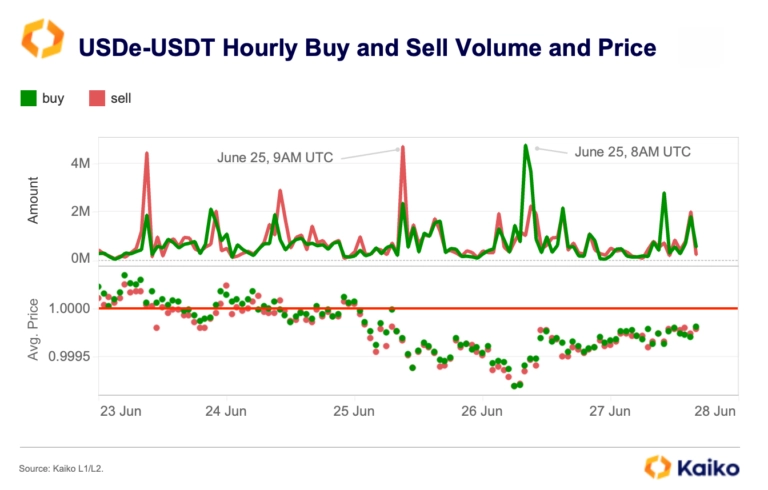

USDe faces regulatory setback in Europe.This week we’re diving into Ethena’s USDe, a stablecoin that’s quickly captured market share and regulatory attention. As global rules tighten and stablecoins become more integrated into mainstream finance, can USDe keep its momentum? We break down the data and the latest headlines.

Written by The Kaiko Research Team![]()

USDC

16/06/2025 Data Debrief

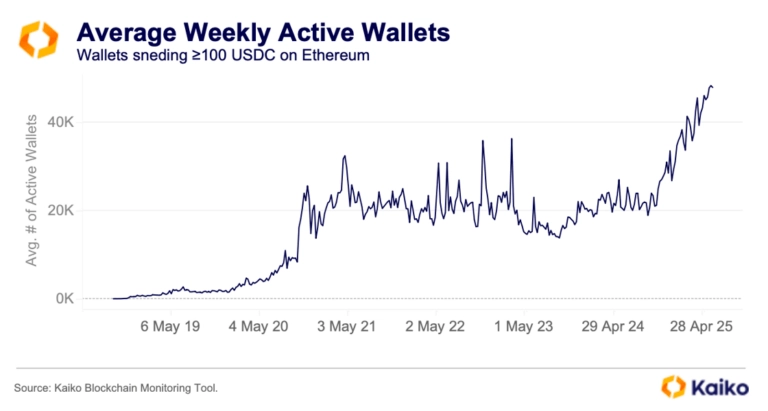

The data behind Circle’s $18B Valuation.Circle’s IPO debut on the New York Stock Exchange on June 5th captured market attention, with shares surging well beyond expectations and outperforming other major crypto listings. This special edition of our Data Debrief examines the on- and off-chain data signals that set the stage for this blockbuster launch and help explain the drivers behind Circle’s remarkable valuation.

Written by The Kaiko Research Team