Sign up for Free Kaiko Research

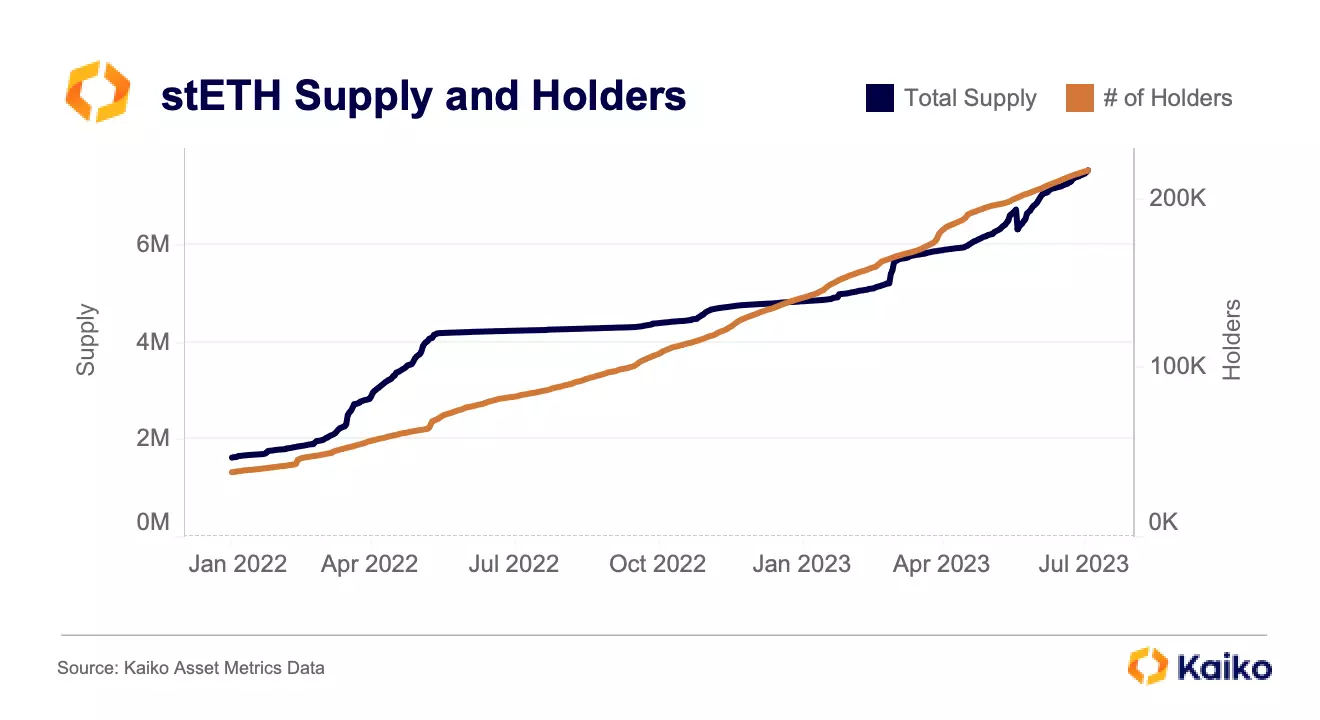

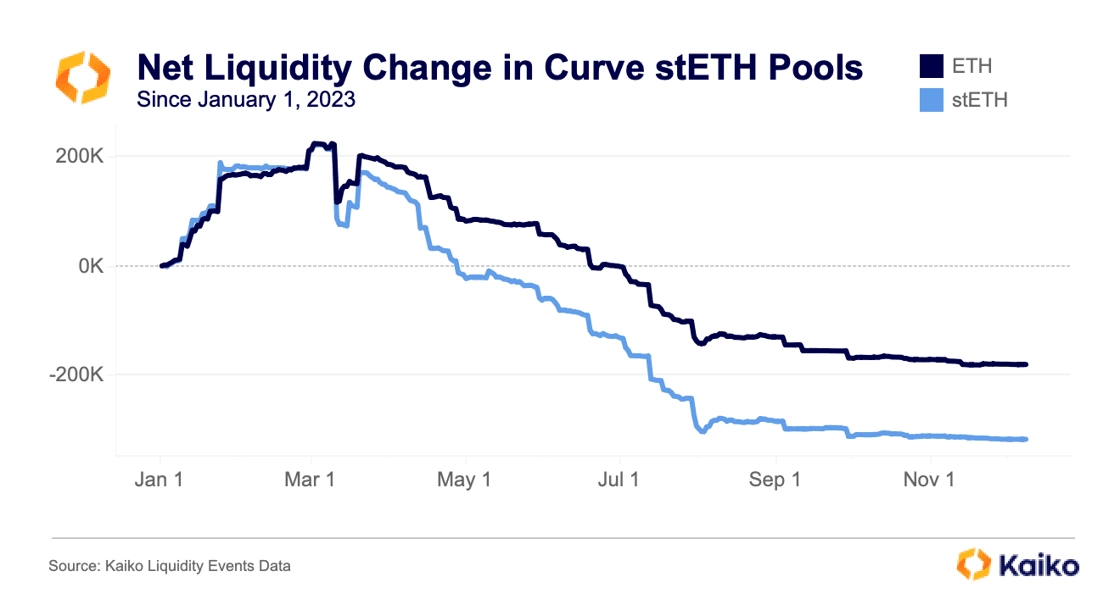

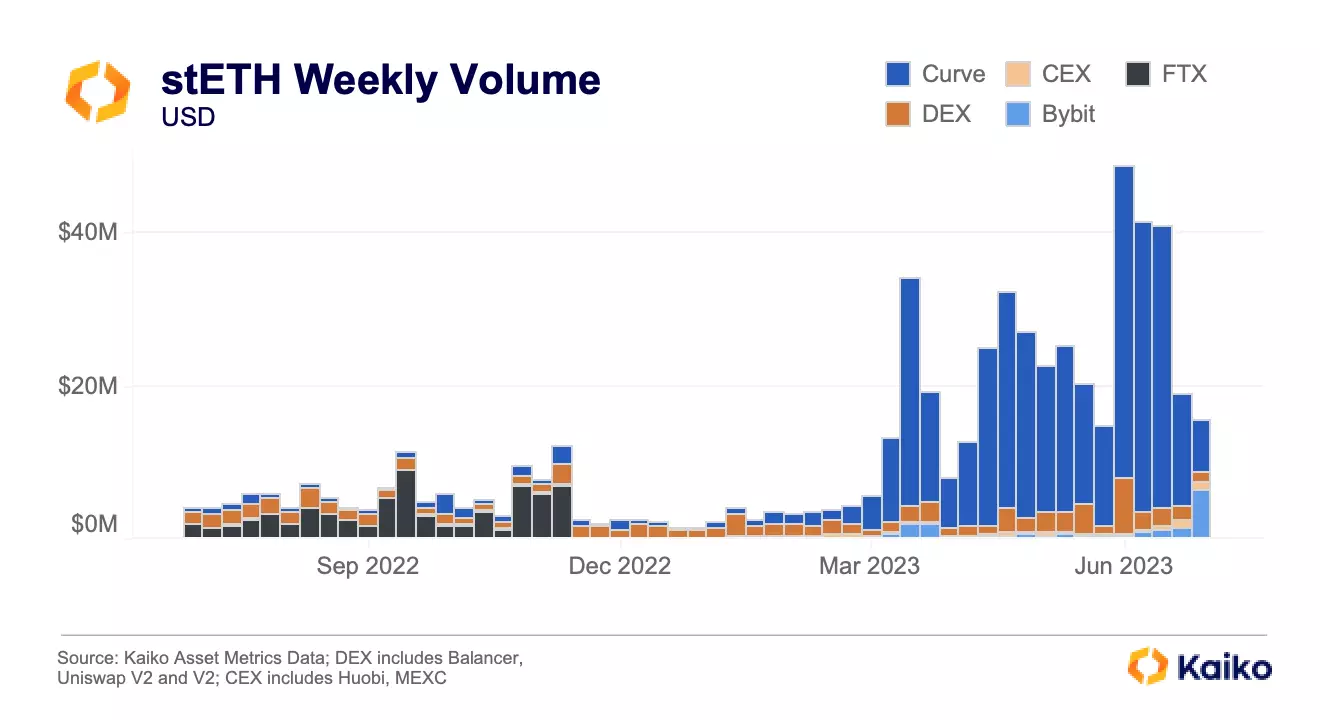

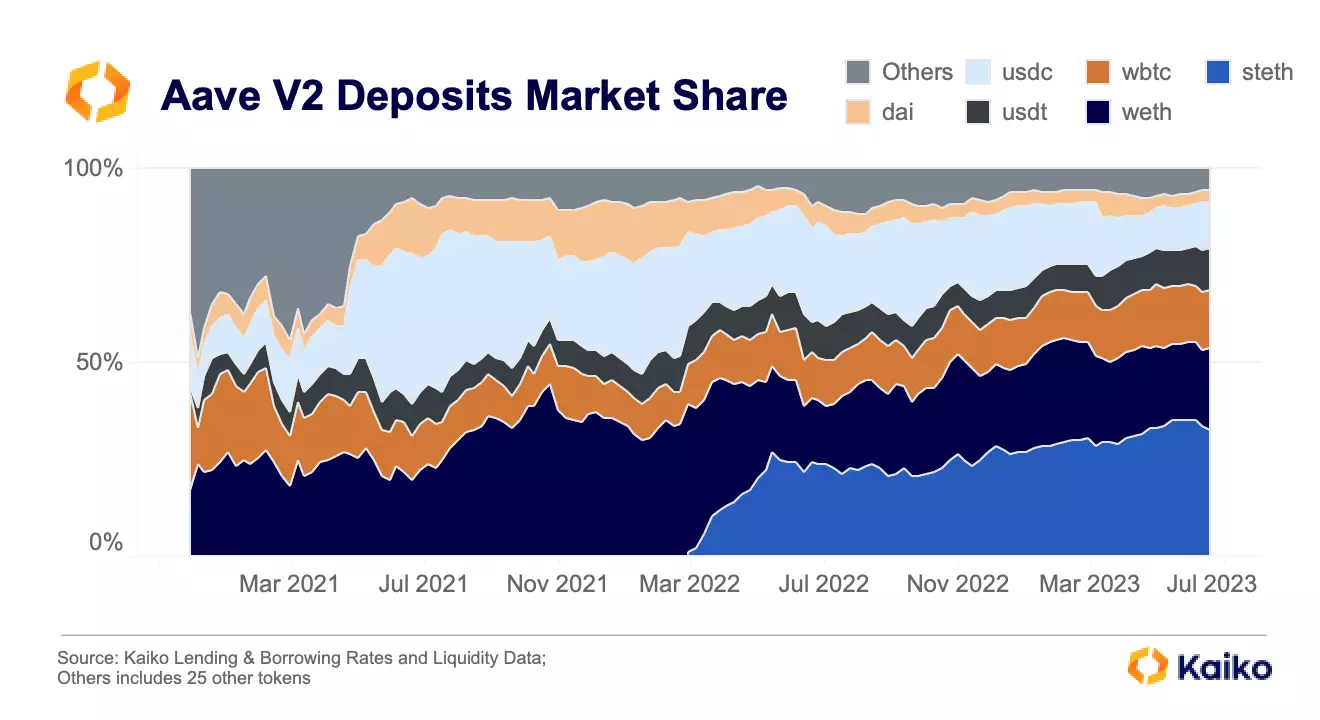

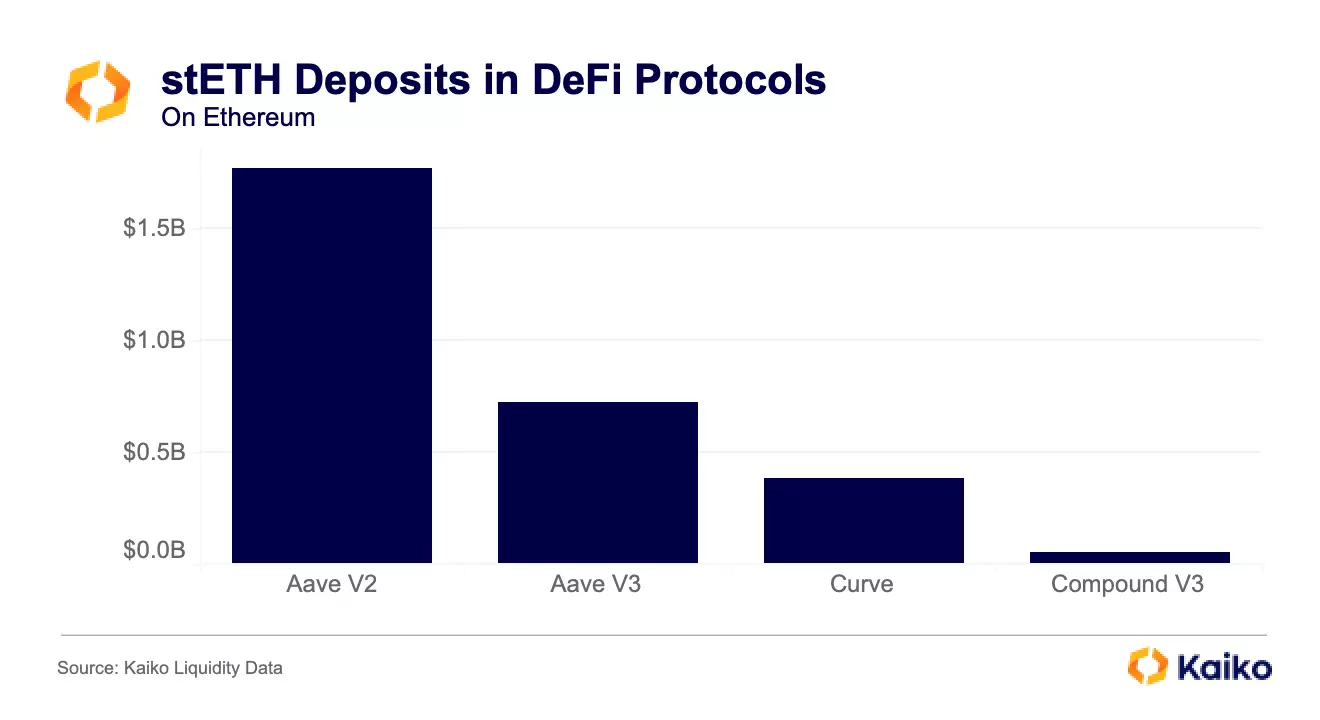

Is stETH Liquid Enough?

Written by Riyad Carey

06/07/2023

Welcome to Deep Dive!

Three Arrows Capital famously blew up because of a series of bad trades, primarily Luna and GBTC. What happened to Luna is obvious: it went to 0 because of UST’s flawed peg maintenance mechanism. The GBTC situation was a bit more complex: “Grayscale allowed big investors like 3AC to purchase shares directly by giving Bitcoin to the trust. These GBTC holders could then sell the shares to the secondary market. That premium meant any sales could net an attractive profit for the big investors.” However, “shares bought directly from Grayscale were locked up for six months at a time. And starting in early 2021, that restriction became a problem. GBTC’s price slipped from a premium into a discount,” which was especially devastating for firms like 3AC, which used leverage to enhance its returns.

Essentially, 3AC made a bet that GBTC – a fundamentally different asset than BTC, with significant frictions in entrance and exit – would closely track BTC’s price. This saga has been front of mind as I’ve observed stETH (and other liquid staking derivatives) begin to displace ETH in DeFi protocols.

More From Kaiko Research

![]()

Hyperliquid

09/03/2026 Data Debrief

Bitcoin Ranges While Traditional Assets Find New Home on Crypto RailsAs Bitcoin ranges between $60k and $72k following the early February sell-off, the crypto market navigates competing forces, with geopolitical shocks testing 24/7 infrastructure and options markets pricing elevated volatility into the Federal Reserve’s March 18th decision.

Written by Laurens Fraussen![]()

Ethereum

02/03/2026 Data Debrief

The Pressure of Dilution on Layer 1 ValuationsAs Layer 1 tokens are increasingly traded through ETFs and evaluated like equity investments, the market is discovering an uncomfortable truth, most major blockchains operate as loss-making businesses. With Ethereum posting $1.62B in annual losses and Solana bleeding $4.15B despite generating hundreds of millions in fee revenue, validator dilution costs consistently outpace income by 7-25x.

Written by Laurens Fraussen![]()

Ethereum

23/02/2026 Data Debrief

Staking Products Launch Despite Treasury FailuresAs crypto volatility continues, the markets are testing whether institutional ETH adoption follows price or infrastructure development. With ETH plunging 50% from its mid-2025 peaks to $2,000, this triggered a 95%+ collapse in equity treasury vehicles like ETHZilla and $4B in spot ETF outflows.

Written by Laurens Fraussen![]()

Prediction Markets

16/02/2026 Data Debrief

Prediction Markets Liquidity In FocusPrediction markets captured mainstream attention throughout 2025 as Polymarket processed over $2 billion in election-related volume. The post-election collapse from $1 billion to $200 million in open interest exposed fundamental questions about sustainability.

Written by Laurens Fraussen