New Report: LATAM's rise in global crypto markets

Q2 Crypto Liquidity Update

Written by Conor Ryder, CFA

15/06/2023

Welcome to Deep Dive!

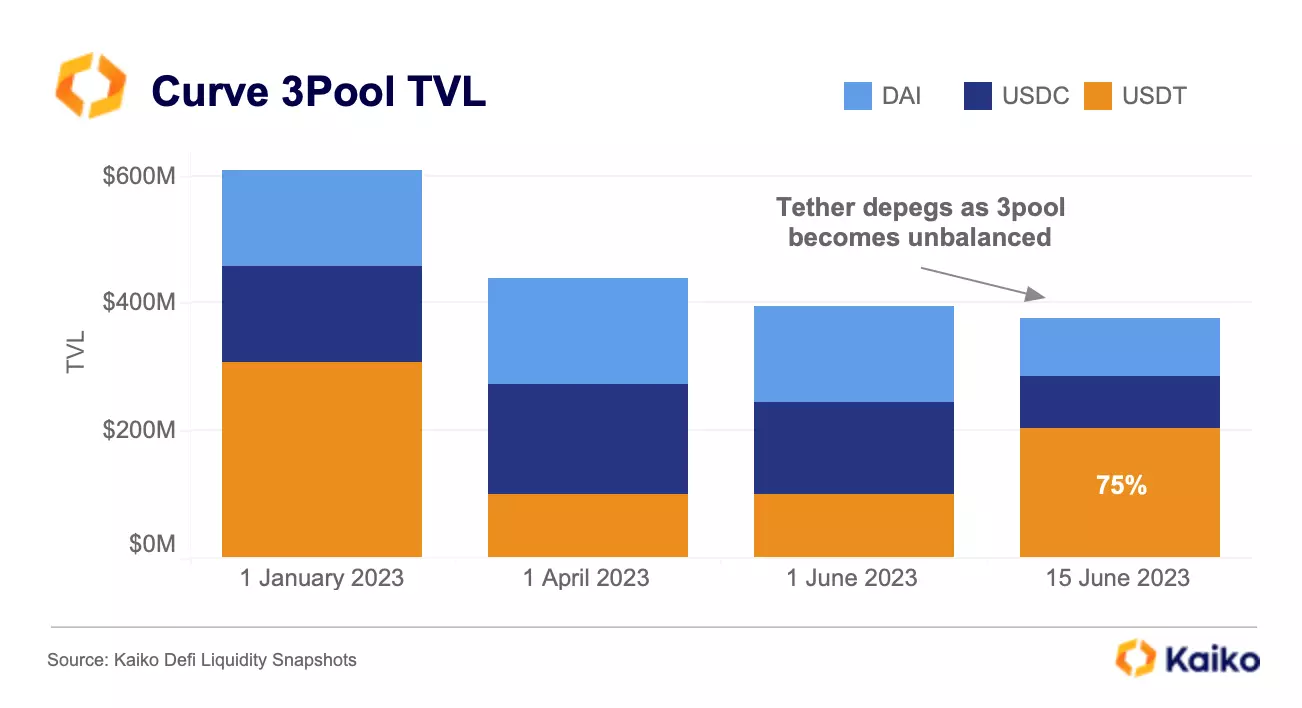

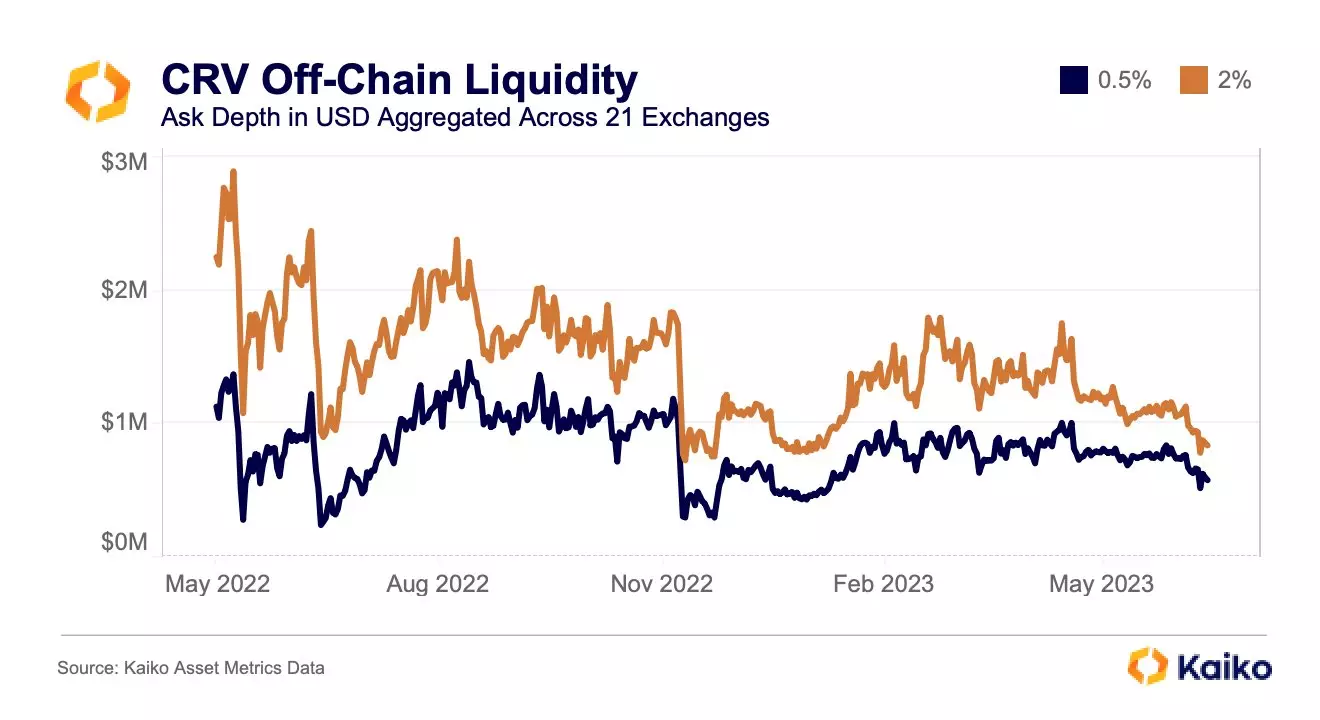

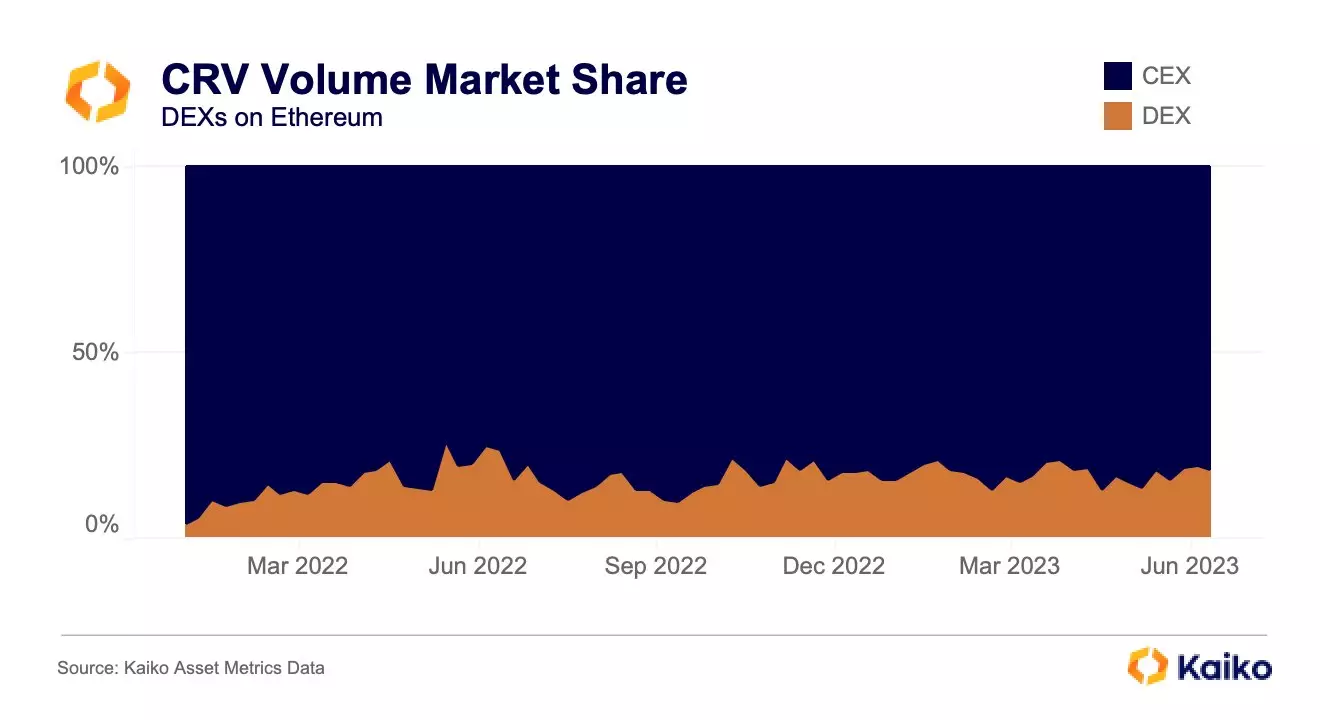

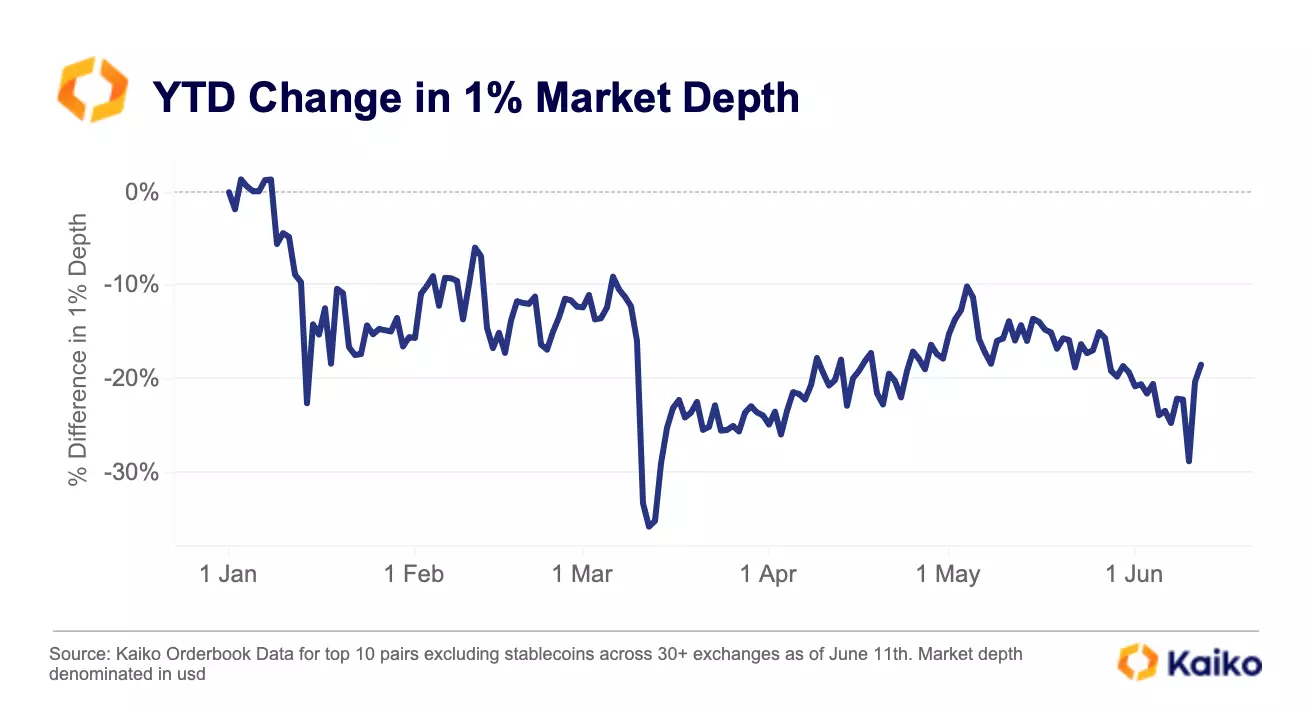

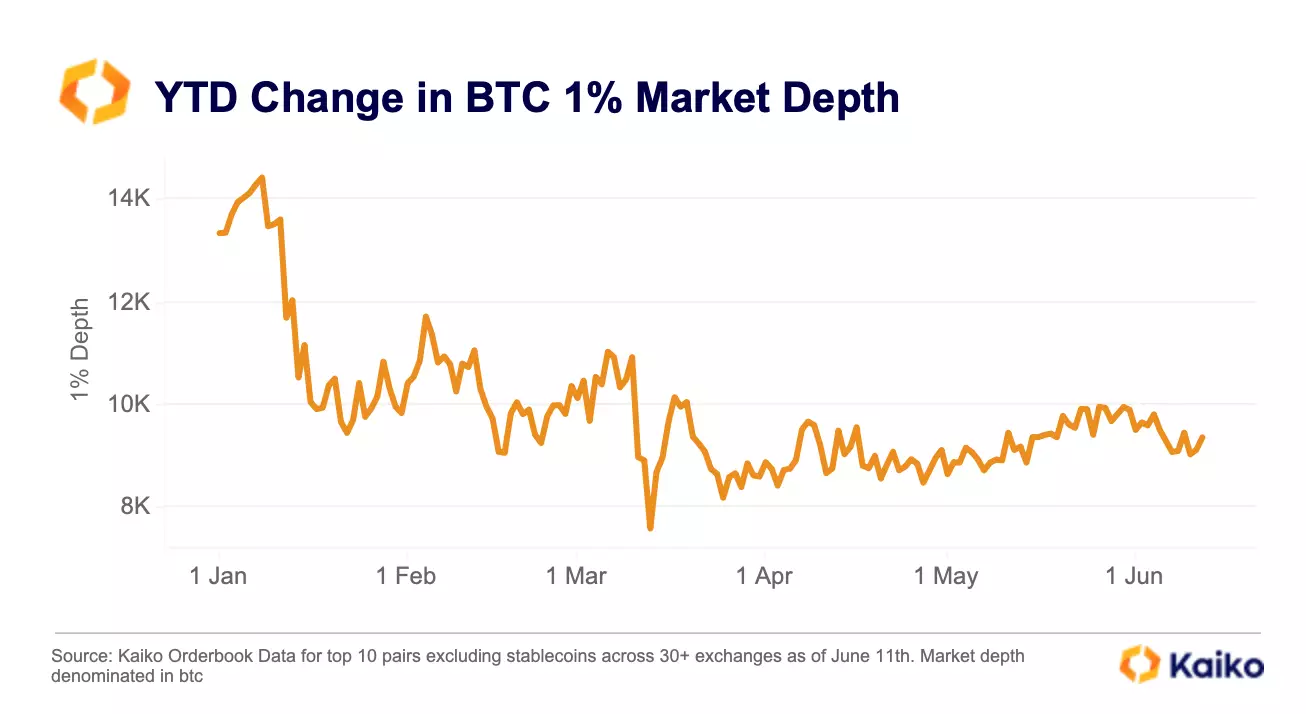

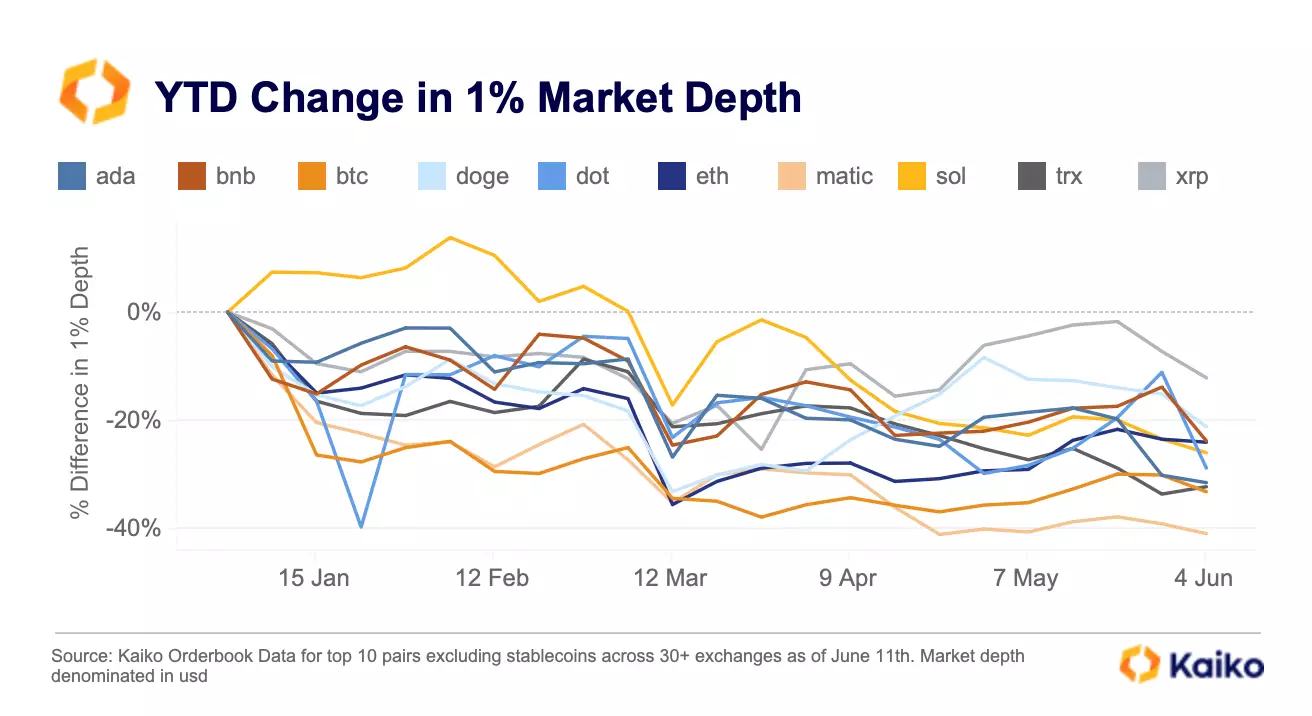

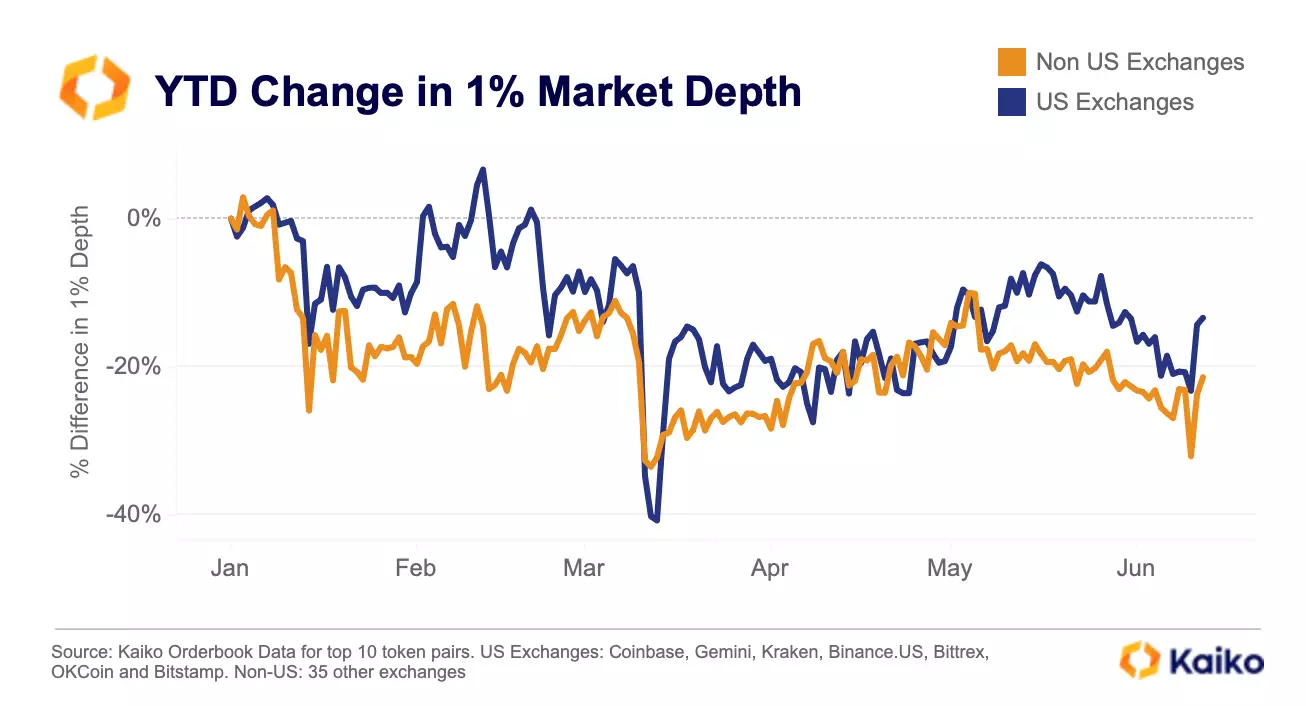

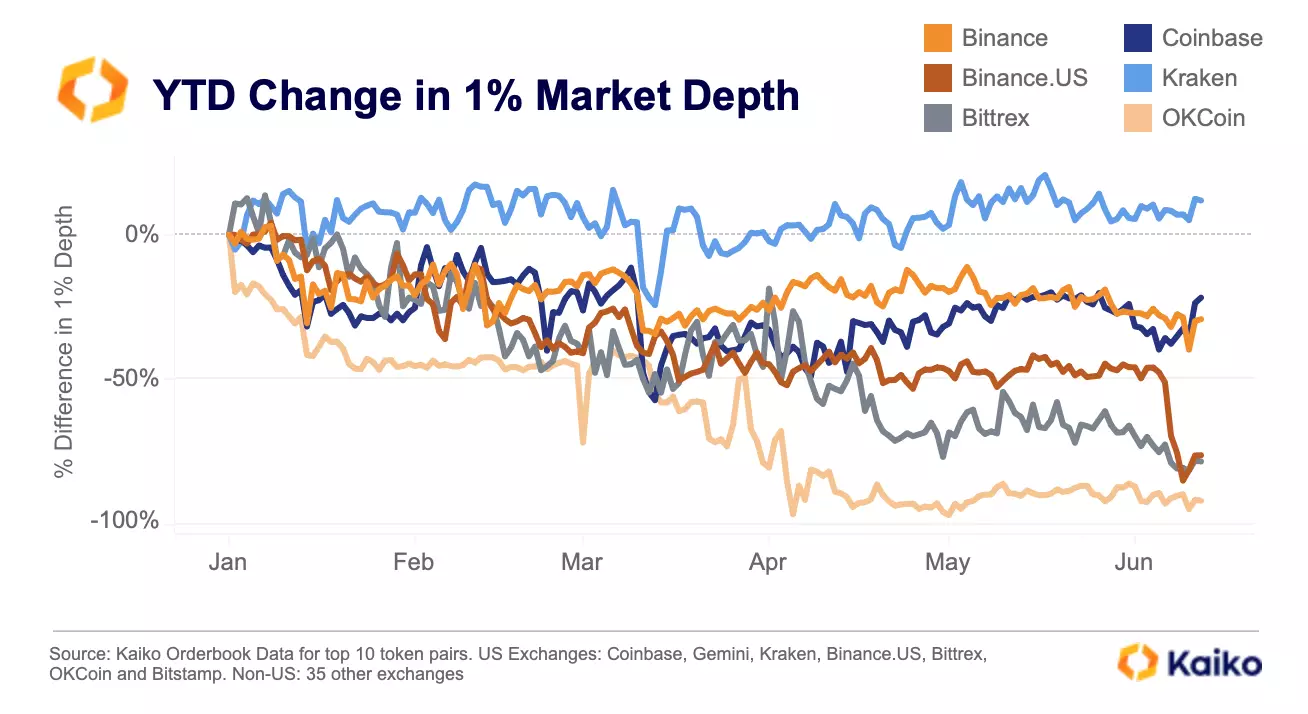

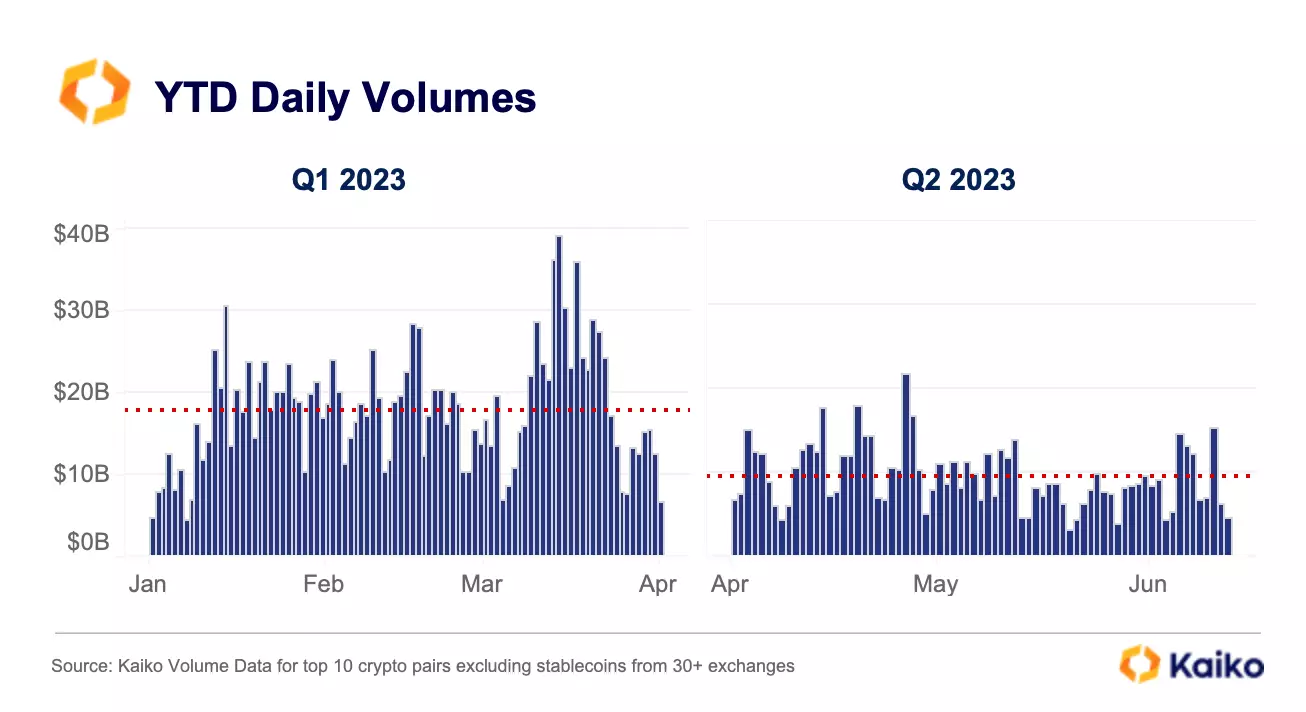

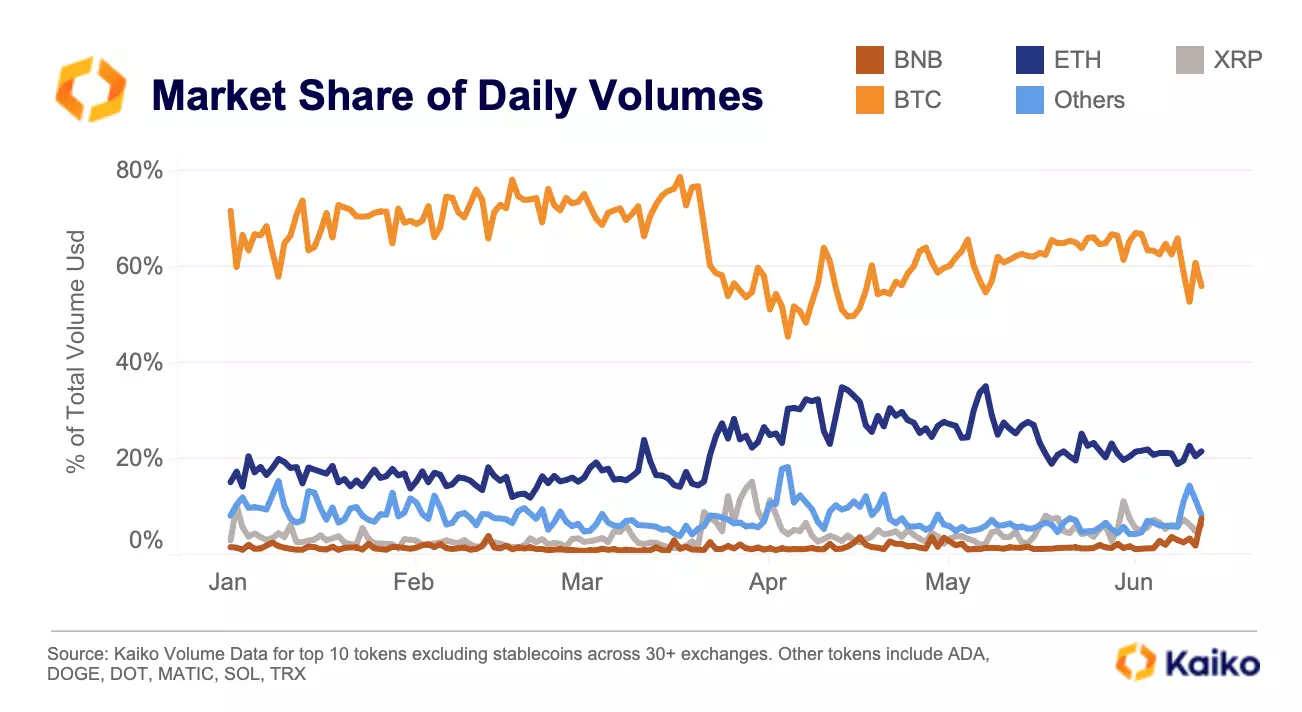

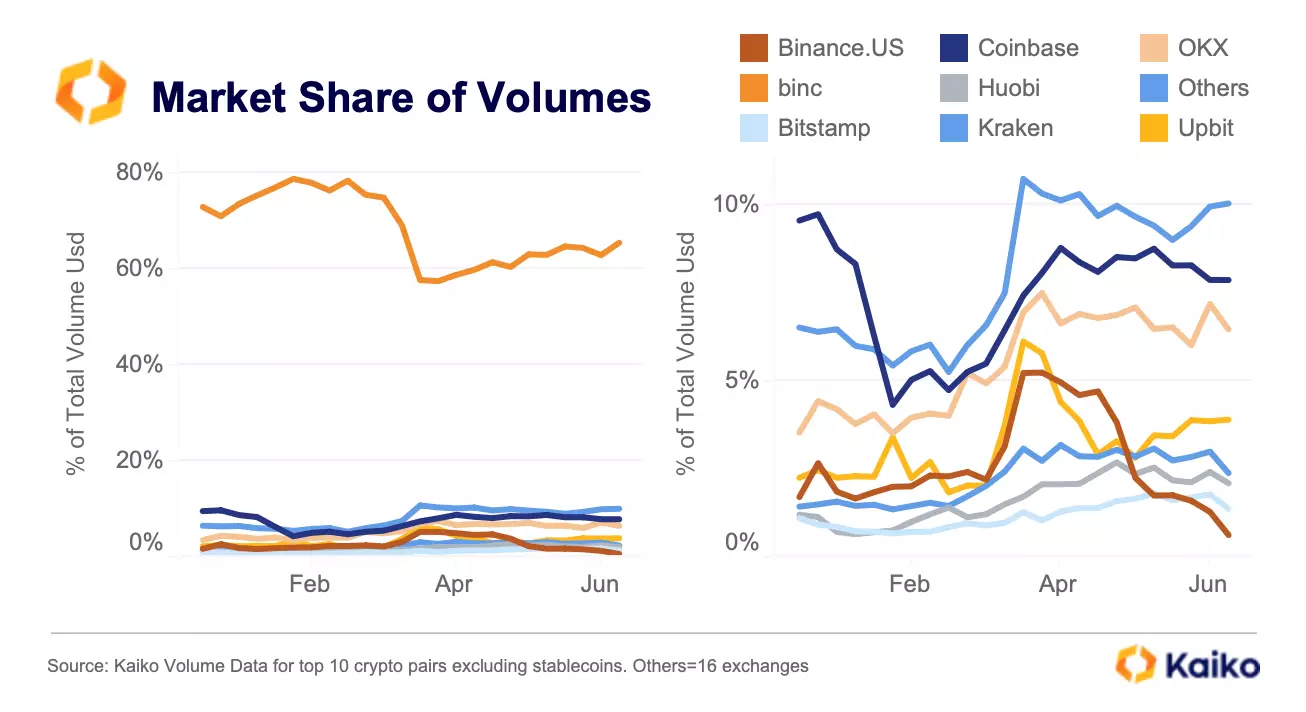

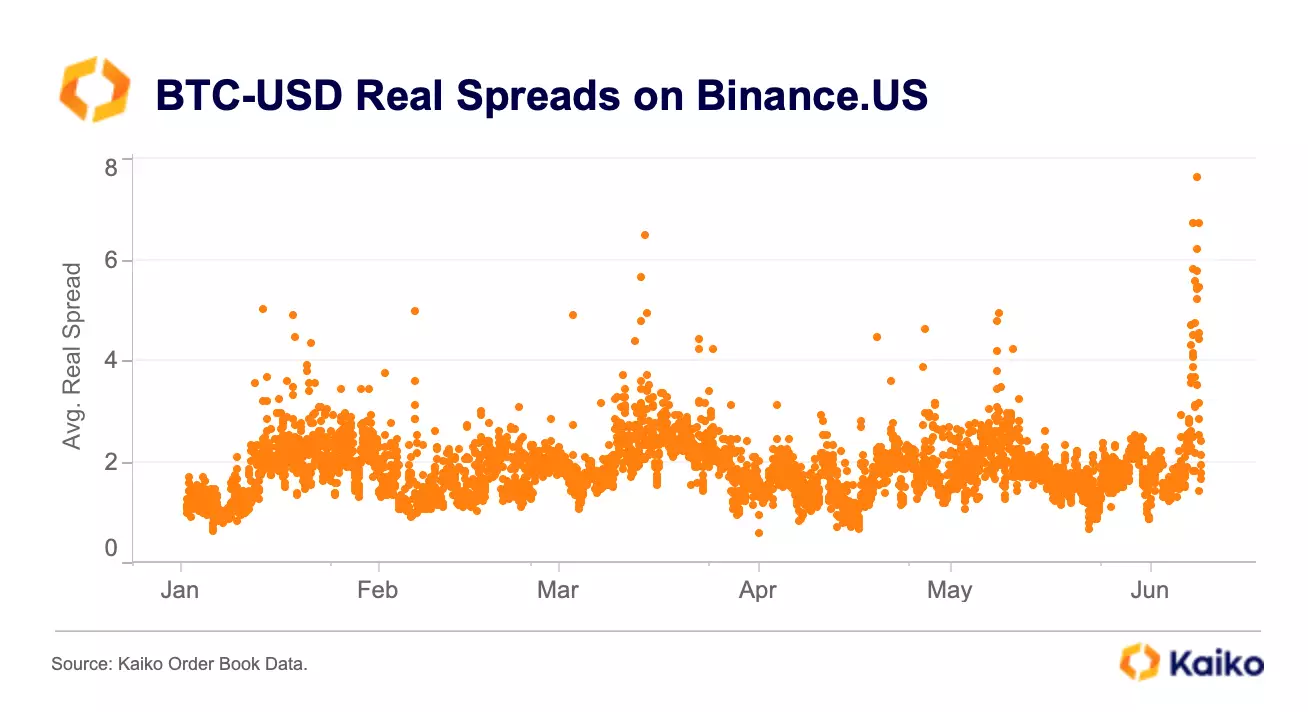

Welcome to Deep Dive! This week we provide a Q2 update on crypto market liquidity, looking at the recent Tether depeg, a big buildup of a CRV position on Aave, and how the SEC’s rulings are impacting centralized liquidity.

More From Kaiko Research

![]()

USDC

30/06/2025 Data Debrief

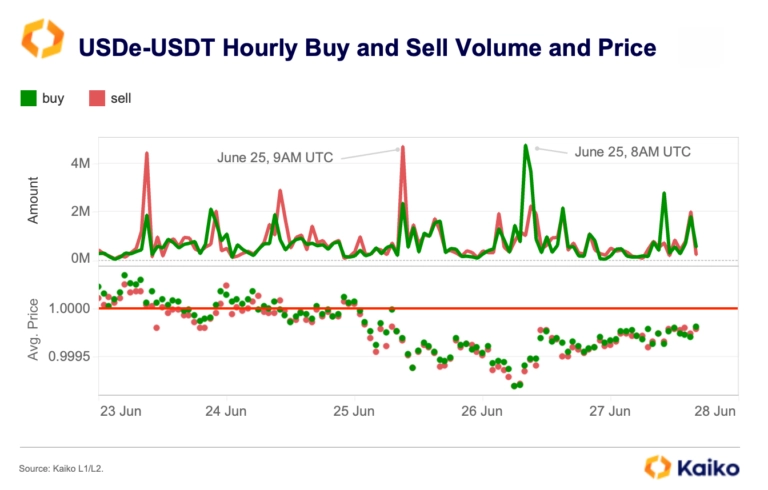

USDe faces regulatory setback in Europe.This week we’re diving into Ethena’s USDe, a stablecoin that’s quickly captured market share and regulatory attention. As global rules tighten and stablecoins become more integrated into mainstream finance, can USDe keep its momentum? We break down the data and the latest headlines.

Written by The Kaiko Research Team![]()

USDC

16/06/2025 Data Debrief

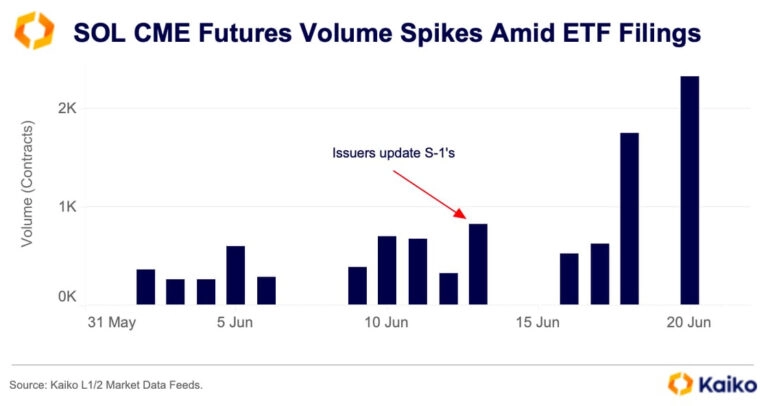

Traders position for potential SOL ETF.This week we’re talking all things Solana. As ETF issuers line up to launch funds tracking SOL the market reaction has been muted in parts. However, looking in the right place shows signs of institutional demand.

Written by The Kaiko Research Team![]()

USDC

16/06/2025 Data Debrief

The data behind Circle’s $18B Valuation.Circle’s IPO debut on the New York Stock Exchange on June 5th captured market attention, with shares surging well beyond expectations and outperforming other major crypto listings. This special edition of our Data Debrief examines the on- and off-chain data signals that set the stage for this blockbuster launch and help explain the drivers behind Circle’s remarkable valuation.

Written by The Kaiko Research Team![]()

CEX

09/06/2025 Data Debrief

Crypto ETFs enter Korea's political mainstreamSouth Korea has a new president, and it’s got big implications for crypto-related exchange-traded funds. Lee Jae-myung won the June 3 election, succeeding Yoon Suk Yeol, who caused market turmoil last year by briefly imposing martial law.

Written by The Kaiko Research Team