New Report: LATAM's rise in global crypto markets

BTC Rally Tracks Softer USD

Written by The Kaiko Research Team

11/08/2025

Welcome to the Data Debrief!

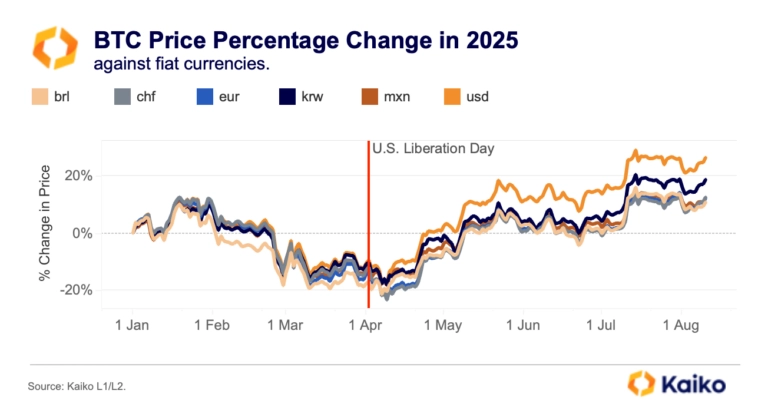

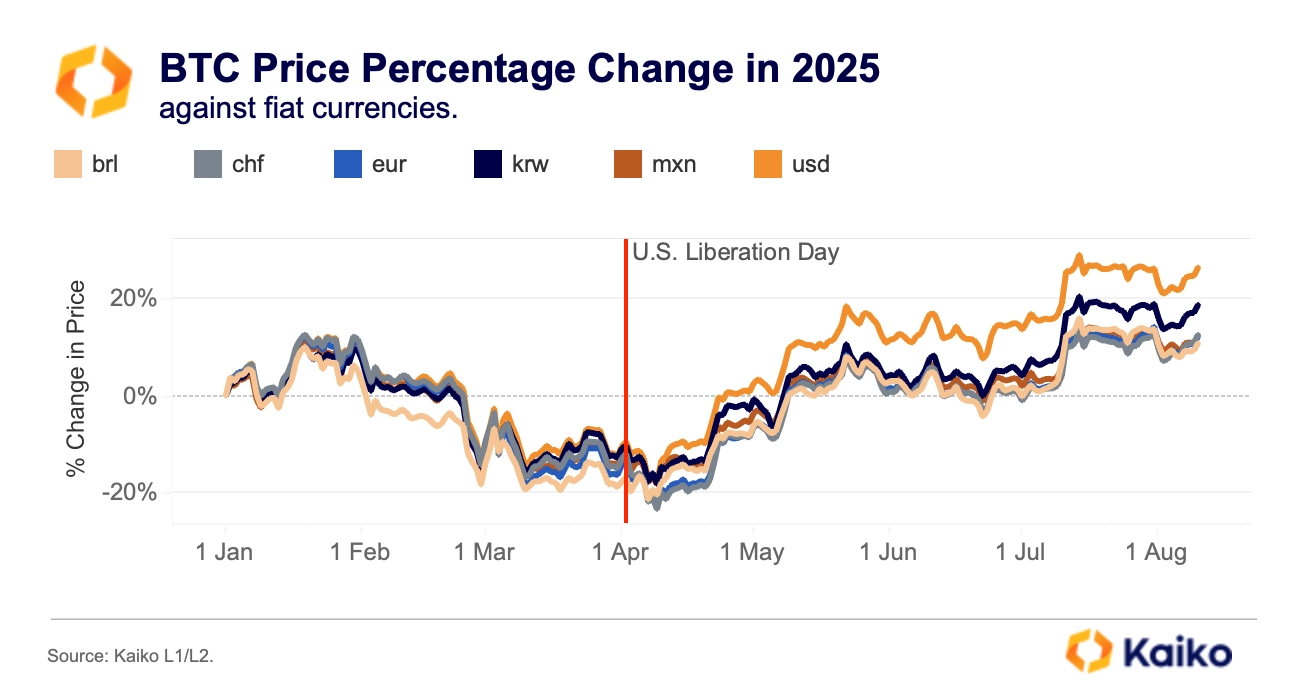

Welcome back to the Data Debrief! Bitcoin pushed back toward its all-time high near $123k early Monday after rebounding from early August lows around $112k. The move tracked a broader risk rally as markets priced a September Fed cut. Stephen Miran’s nomination to the Fed Board last week reinforced that view after weak July jobs data. A softer dollar added a tailwind, lifting USD‑quoted flows and amplifying BTC’s gains.

Data Used In This Analysis

Our industry-leading research is the direct result of combining our proprietary data with world-class in-house experts. Bringing the very best of Kaiko’s people and data together, we unlock the unique insights that form the basis for our discoveries and analysis. We believe in doing so, our data speaks for itself, helping both our clients and the wider industry get a better understanding of the crypto ecosystem, and the evolving trends and patterns in motion at a regional and global scale.

More From Kaiko Research

![]()

Bitcoin

25/08/2025 Data Debrief

ETH breaks out on strong spot demand.ETH broke its 2021 all-time high over the weekend, reaching as high as $4,996 on some cryptocurrency exchanges and outperforming BTC in both price and volume. It later eased to around $4.6k on Monday, but volumes remain strong, indicating the rally still has momentum.

Written by The Kaiko Research Team![]()

Bitcoin

18/08/2025 Data Debrief

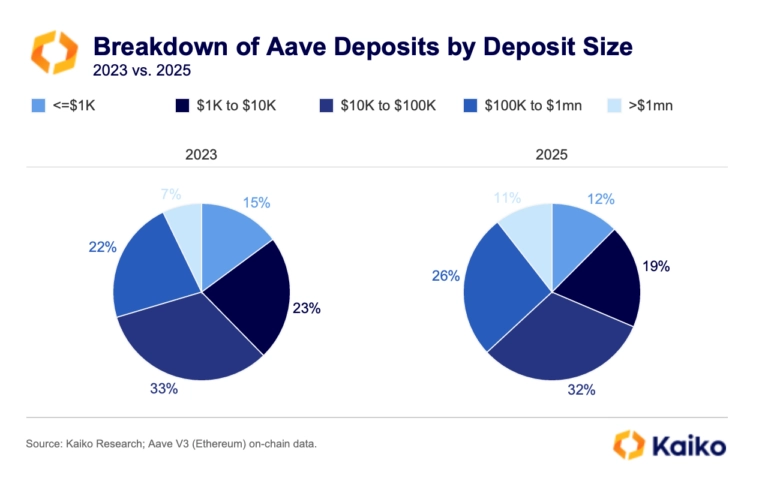

Mapping the AAVE User Base.Better on-ramps and embedded swaps are bringing more people on-chain. But DeFi lending and leverage still sit with a small group of large, sophisticated users. In this special edition we map Aave’s user base by deposit size, activity, collateral choices, and risk posture to understand who powers the protocol and what that implies for liquidity, stability, and growth.

Written by Louis Latournerie![]()

Bitcoin

11/08/2025 Data Debrief

BTC Rally Tracks Softer USD.Bitcoin pushed back toward its all-time high near $123k early Monday after rebounding from early August lows around $112k. The move tracked a broader risk rally as markets priced a September Fed cut. Stephen Miran’s nomination to the Fed Board last week reinforced that view after weak July jobs data. A softer dollar added a tailwind, lifting USD‑quoted flows and amplifying BTC’s gains.

Written by The Kaiko Research Team![]()

CEX

04/08/2025 Data Debrief

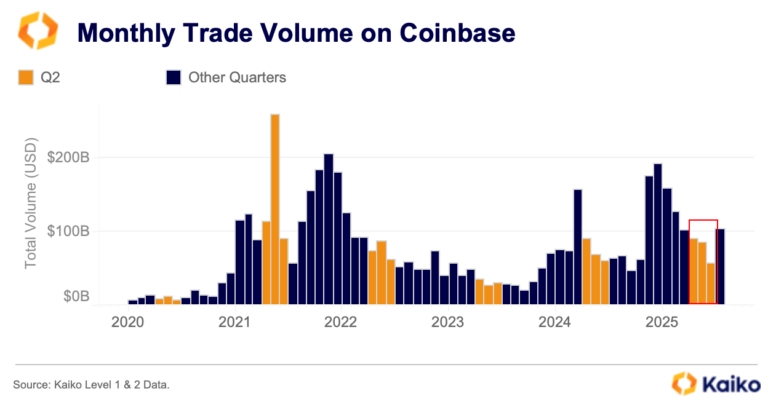

Why Coinbase Wants to be the Everything ExchangeThe bulk of public earnings took place last week, with plenty of crypto-related news to digest. In today’s Data Debrief, we’re focusing on Coinbase’s quarterly results and market positioning, looking at volume share versus competitors, COIN share performance, and the top asset performers on the exchange, along with their quarterly trends and the company’s strategy in becoming the “Everything Exchange.”

Written by Adam Morgan McCarthy