Data Points

TradFi dominates tokenisation trend.

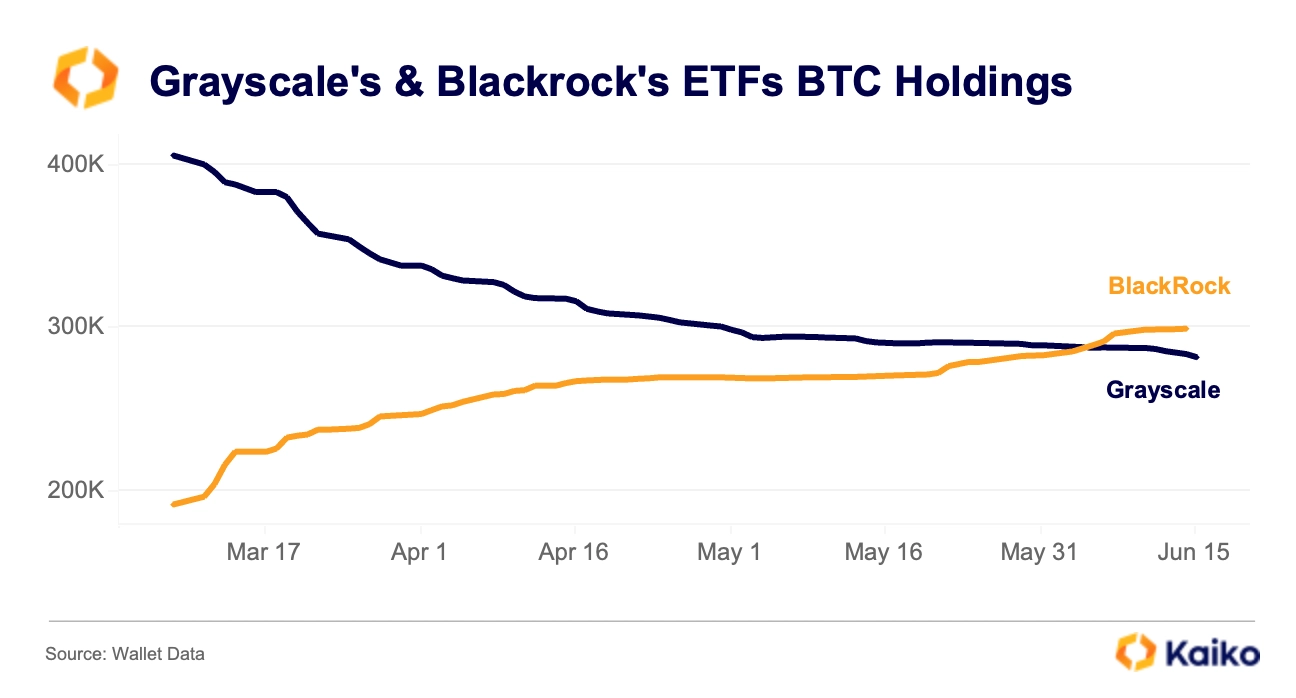

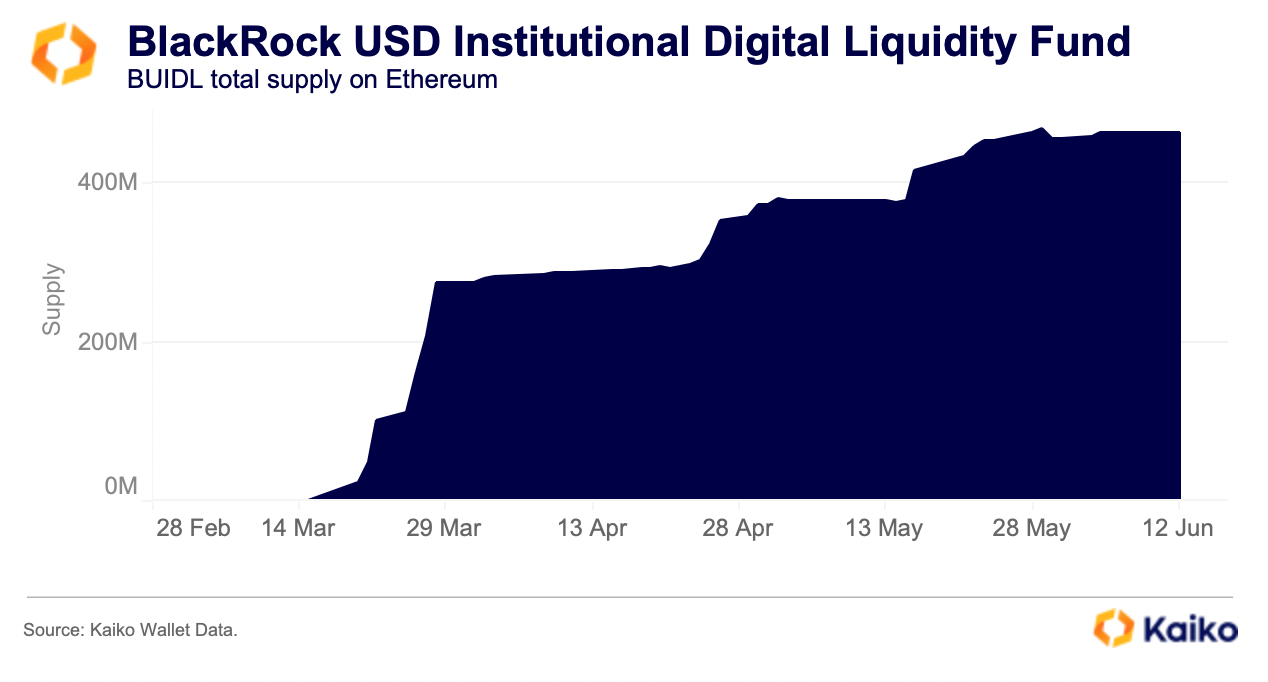

Last week, Fidelity International announced its participation in JPMorgan’s tokenized network, becoming the latest institutional player to join the rapidly growing tokenization trend. In parallel, BlackRock’s BUIDL, its tokenized liquidity fund, continues to grow and has now accumulated over $460 million.

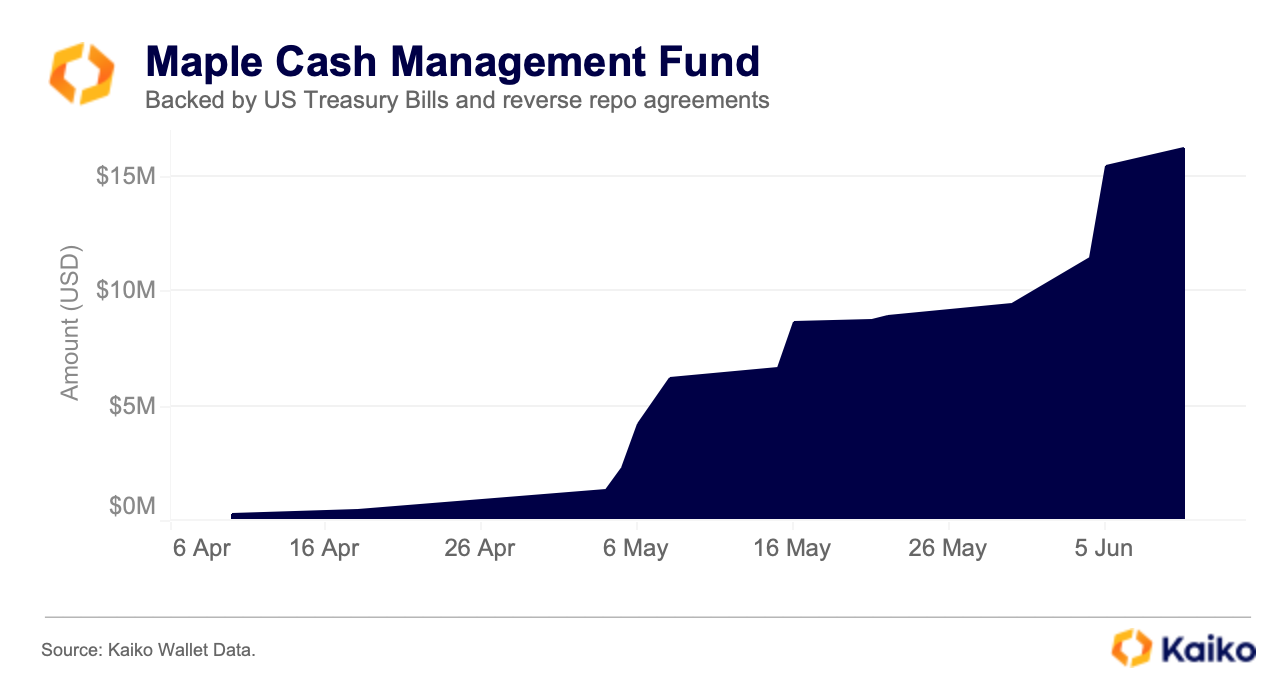

Since its launch in March, BlackRock’s BUIDL has outpaced several crypto-native firms, including Maple Finance’s Cash Management Fund, which focuses on short-term cash instruments. Although Maple has been active in the space for years and recovered from the 2022 crypto lending services collapse, its Cash Management Fund has only amassed around $16 million in assets, paling in comparison to BUIDL.

Meme tokens liquidity improves.

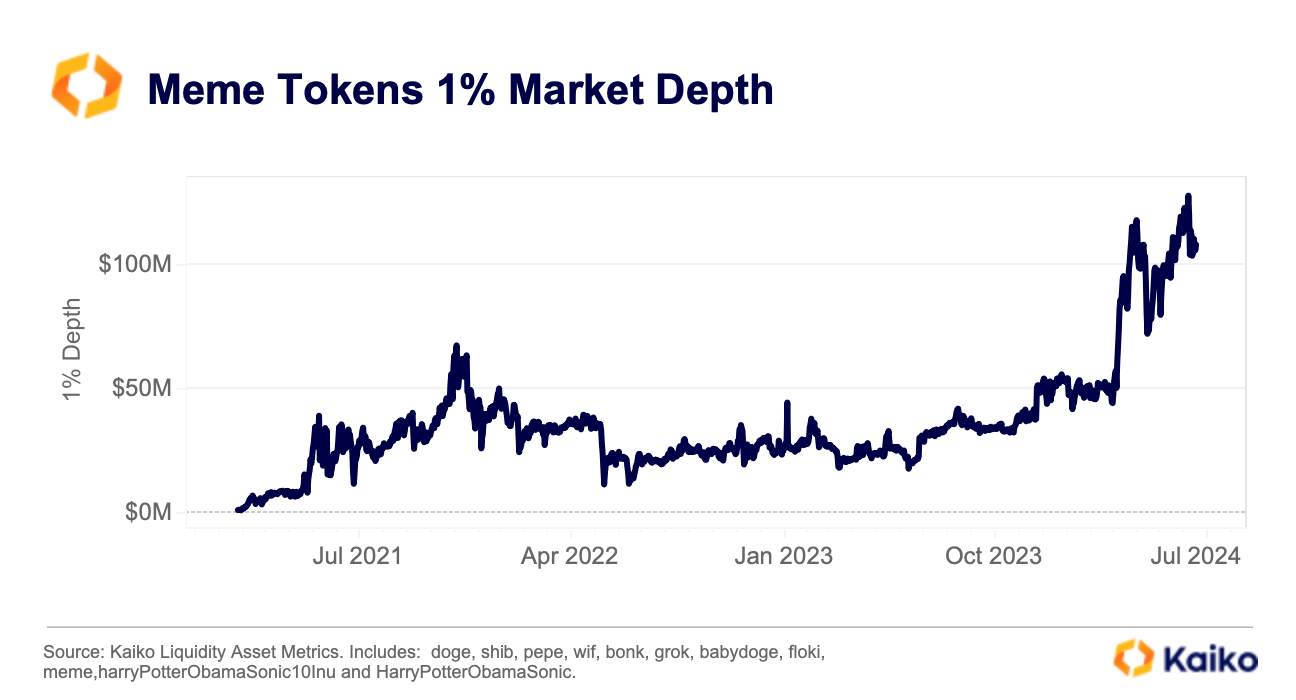

Despite the recent market correction, meme tokens continue to be among the best performers this year, outperforming Bitcoin and other altcoins. Meme tokens liquidity, as measured by the 1% market depth, has also surged, doubling since the start of the year. It reached an all-time high of $128 million in early June before retreating slightly.

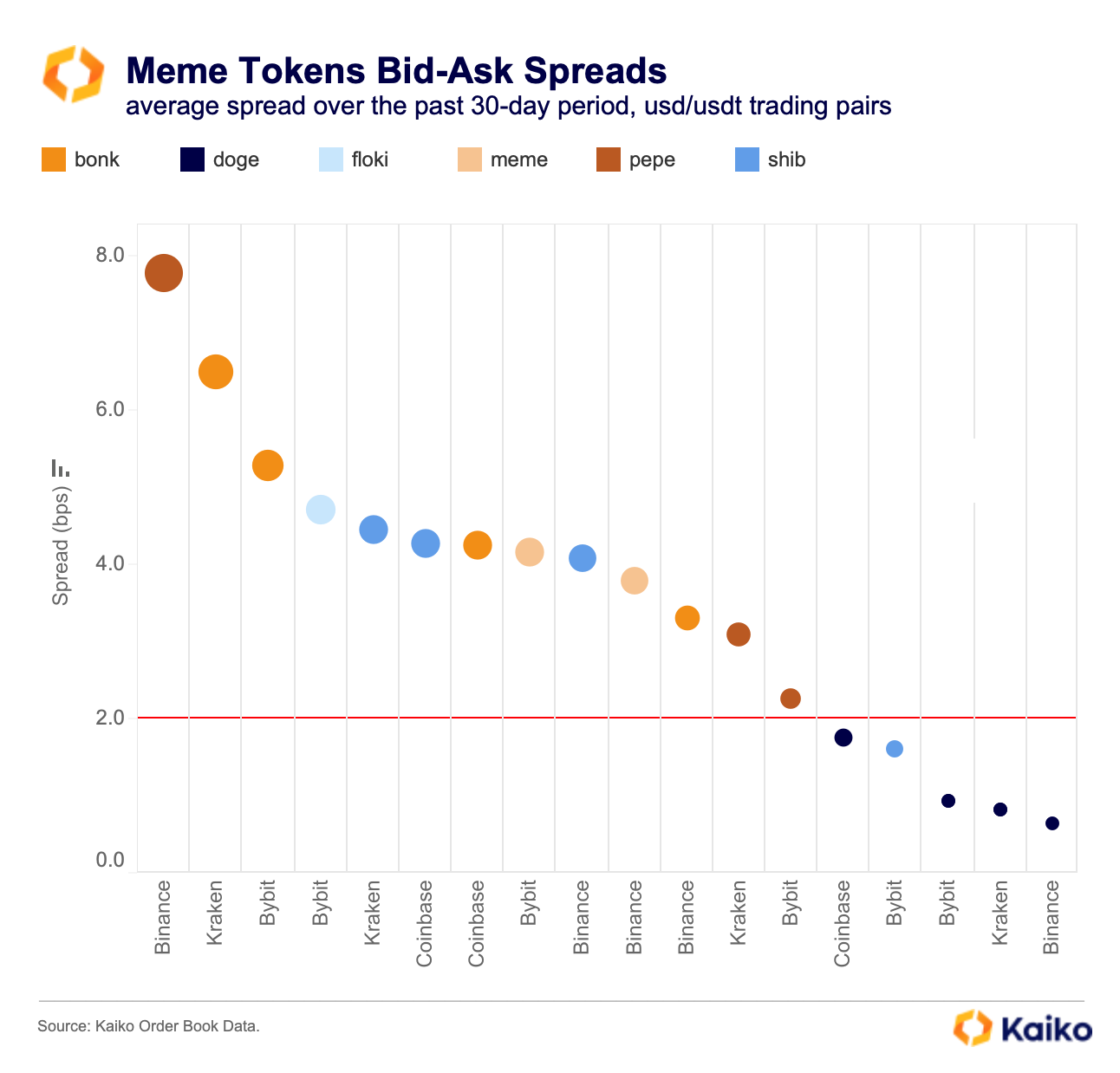

While part of this increase is related to price appreciations, many small-cap meme tokens such as Dogwifhat (WIF), Memecoin (MEME), or Book of Meme (BOME) have seen significant growth in liquidity in native units, ranging from 200% to 4000%. However, the cost of trading these tokens remains high, with bid-ask spreads exceeding 2 basis points on most exchanges.

This suggests that while more market makers are venturing into providing liquidity for these tokens, they are still considered risky due to their high volatility. As we noted earlier, the price discovery of meme tokens is relatively more focused on derivative markets, making them prone to cascading liquidations, which can exacerbate price swings.

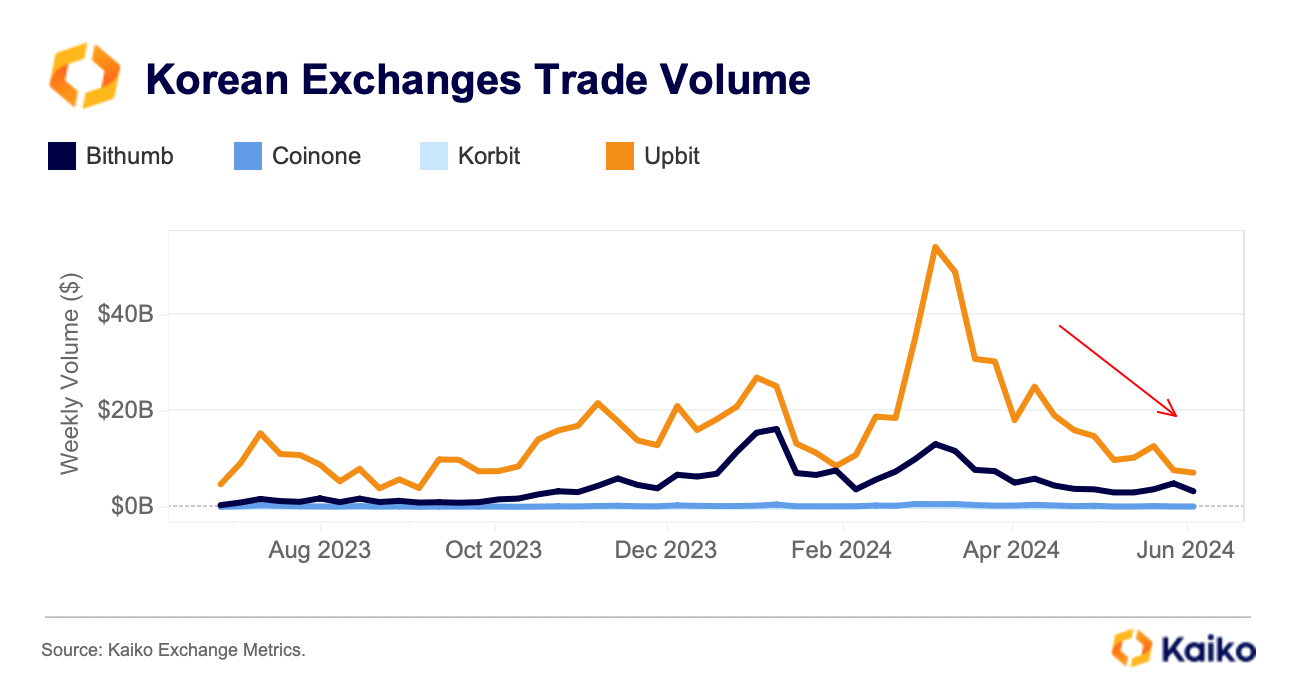

Korean exchanges lose steam.

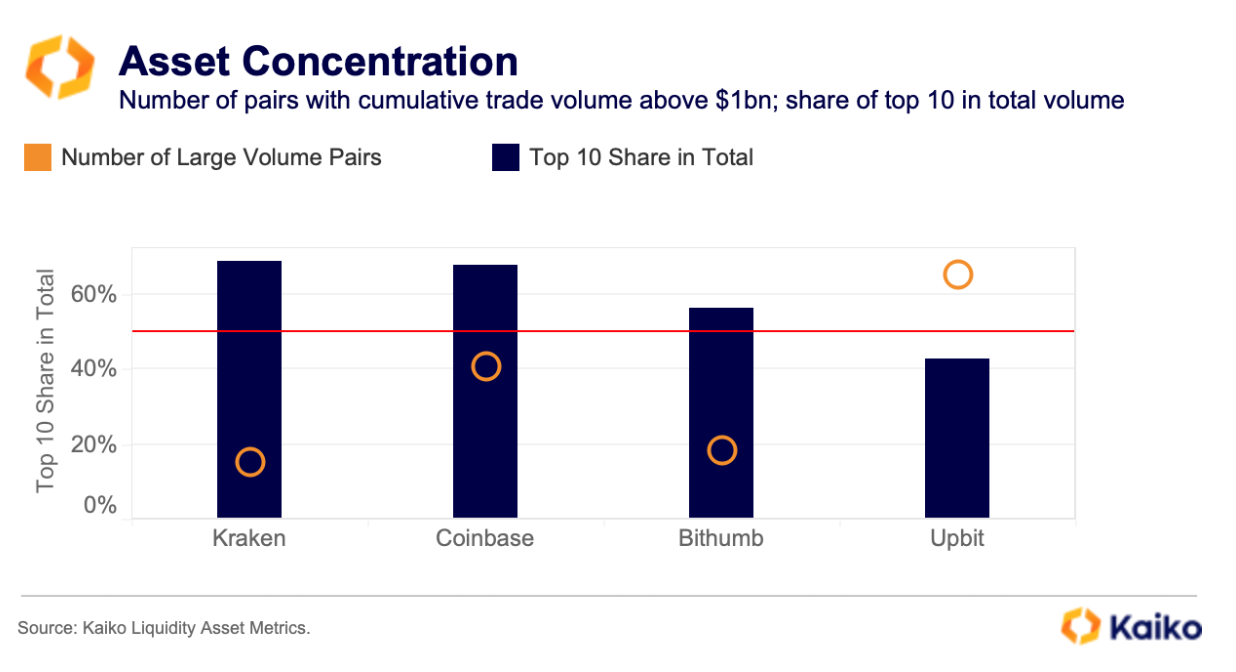

After briefly surpassing USD trade volume in Q1, Korean Won (KRW) trade volume has slowed markedly in Q2. The weekly trade volume on the four major Korean exchanges—Upbit, Bithumb, Coinone, and Korbit—has declined to $6 billion in early June from an average of $35 billion in Q1. The decline was particularly strong on Upbit, which has seen its market share relative to its main local competitor, Bithumb, retreat to 67%, its lowest level since February.

One explanation for the decline could be softening risk sentiment following stickier than anticipated inflation in the US and a repricing in Fed rate cuts expectations. Upbit and Bithumb both offer a higher number of large volume trading pairs than other exchanges. The top ten pairs by cumulative volume accounted for only 43% of Upbit’s trade volume, compared to 70% on Coinbase and Kraken.

However, as we mentioned in our Deep Dive on liquidity this does not always correlate with better liquidity conditions. Many of the most popular assets are small-cap altcoins driven by swings in speculative interest.

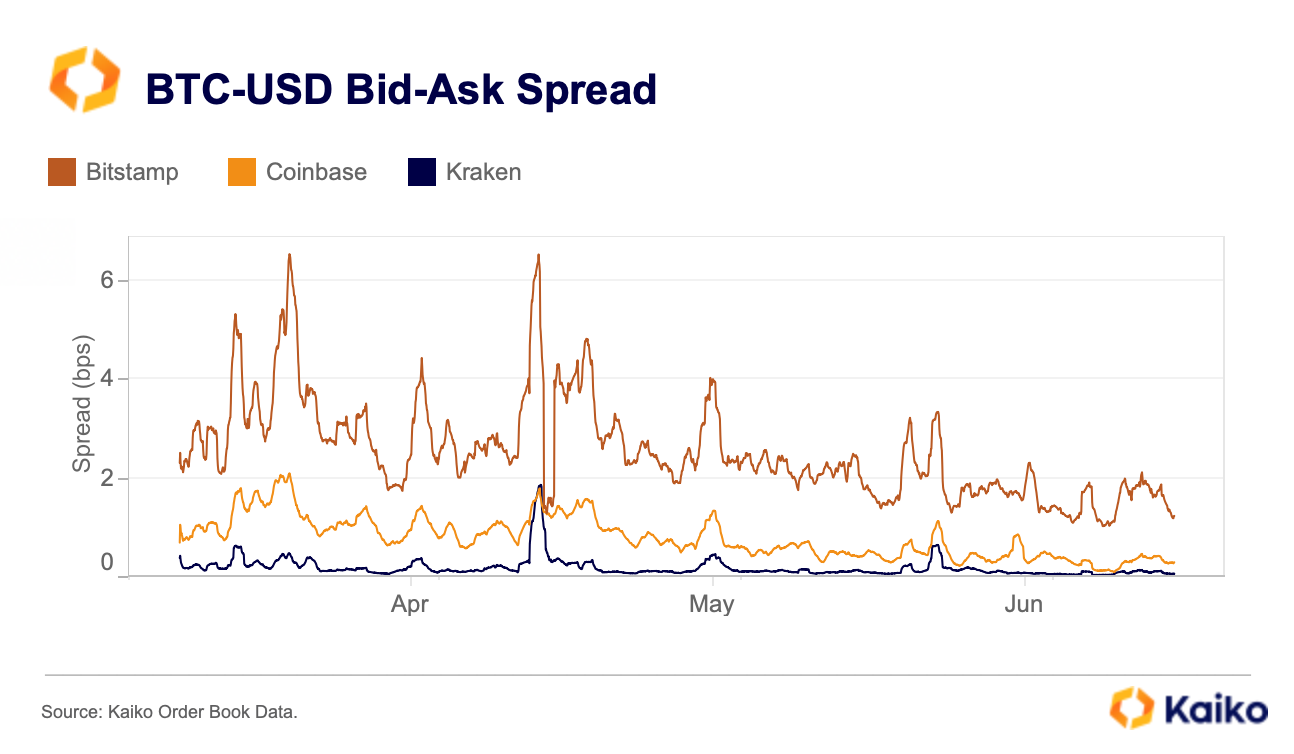

Liquidity is improving on US exchanges.

The bid-ask spread on major US exchanges has significantly decreased, indicating better liquidity for bitcoin. The spread represents the difference between the highest buyer’s price and the lowest seller’s price, with smaller spreads signaling a more liquid market. Spreads have fallen from 2.3 to 1.9 basis points on Bitstamp, over 1 to 0.3 basis points on Coinbase, and 0.4 to 0.1 basis points on Kraken.

The introduction of spot BTC ETFs likely contributed to this trend, as other liquidity indicators like market depth also improved. This liquidity enhancement is beneficial, considering Q3 has historically seen the lowest Bitcoin trading volumes.

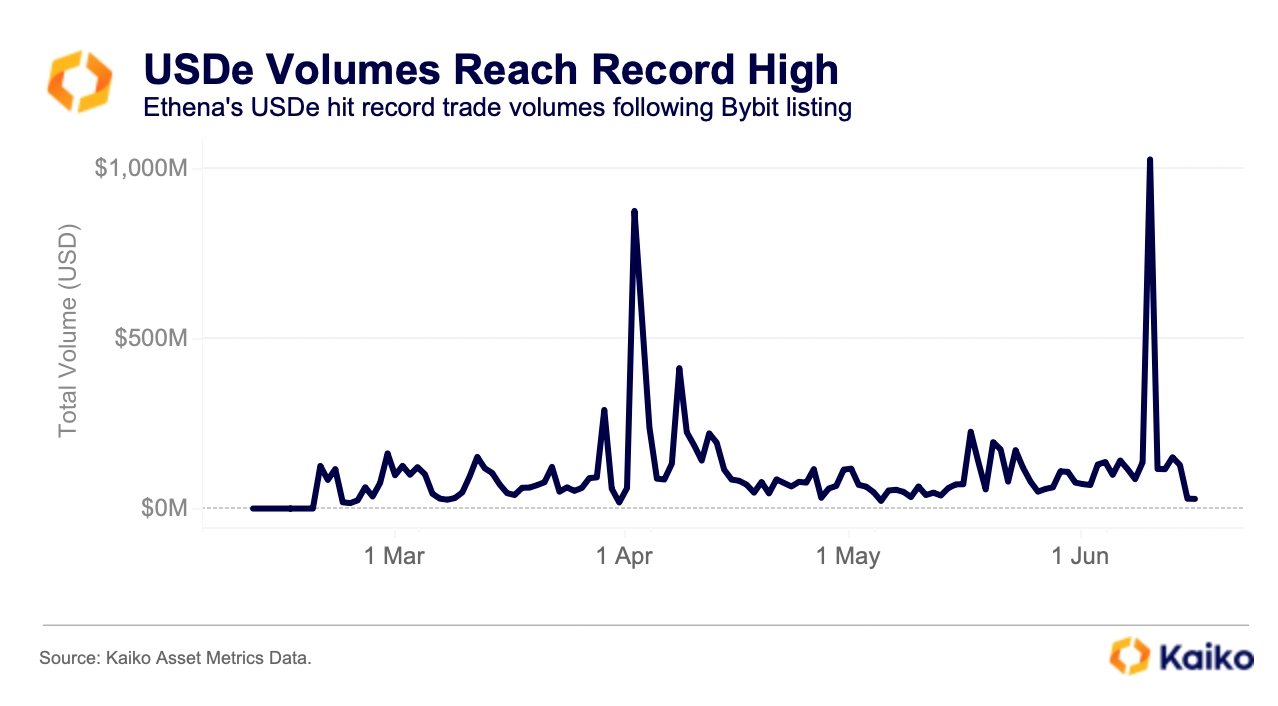

USDe volumes soar on Bybit listing.

Ethena’s USDe ‘synthetic dollar’ recorded its best 24 hours of trading volume on record last week as it launched multiple trading pairs on Bybit.

Bybit users can trade BTC and ETH using USDe for zero-fees as part of its launch on the platform. Trading volumes spiked to over $1bn following the launch, surpassing USDe’s previous 24-hour record of $870mn set on April 2 as early adopters claimed the ENA airdrop.

The spike in volume was somewhat similar to the launch of FDUSD zero-fee trading pairs on Binance. However, USDe volumes didn’t sustain beyond the first day of trading, unlike FDUSD, and volumes fell to around $127mn by Friday.