Now Available: Q2 2024 Crypto Market Report

Breaking Down Worldcoin’s Launch

Written by Riyad Carey

27/07/2023

Welcome to Deep Dive!

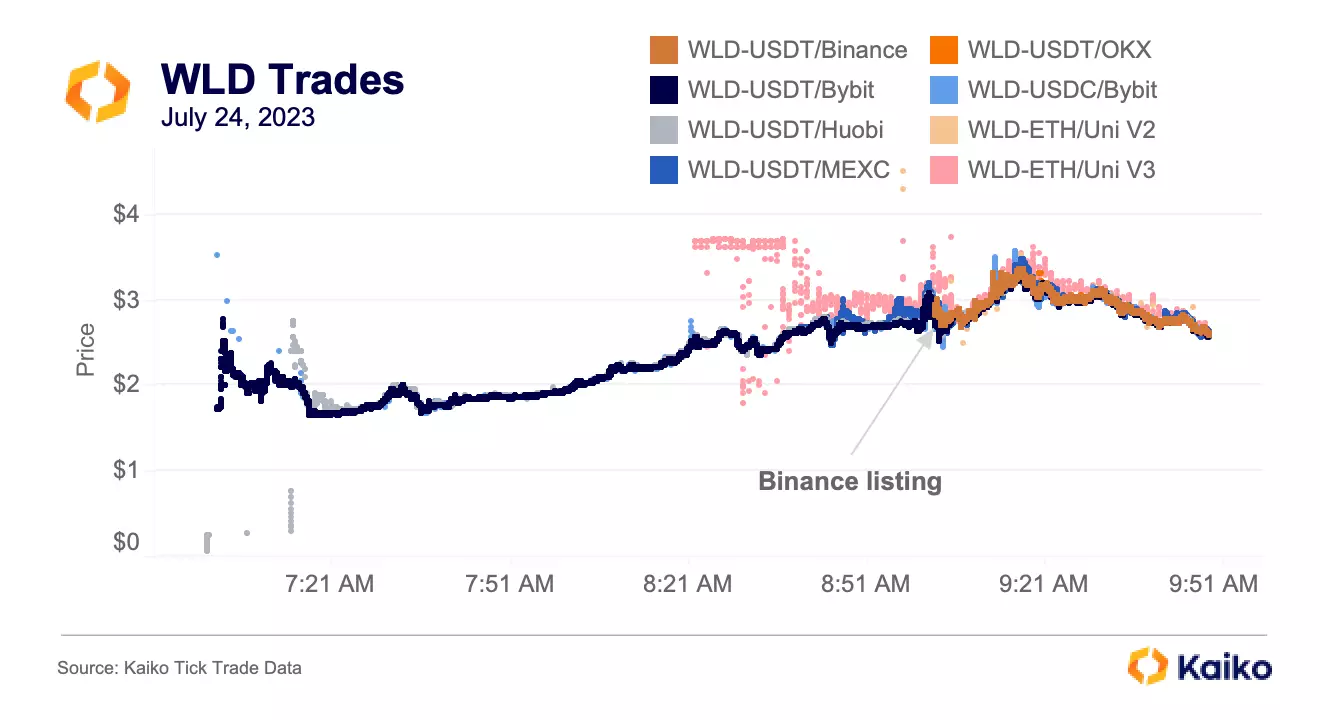

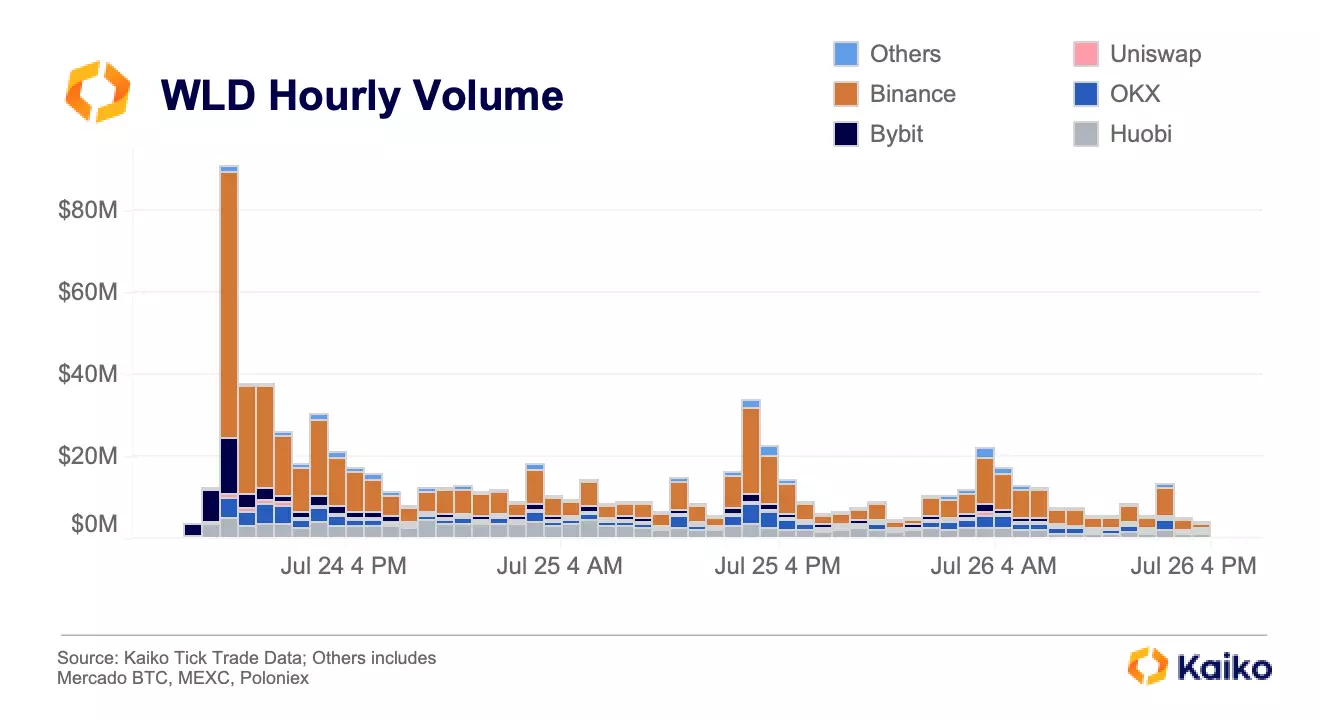

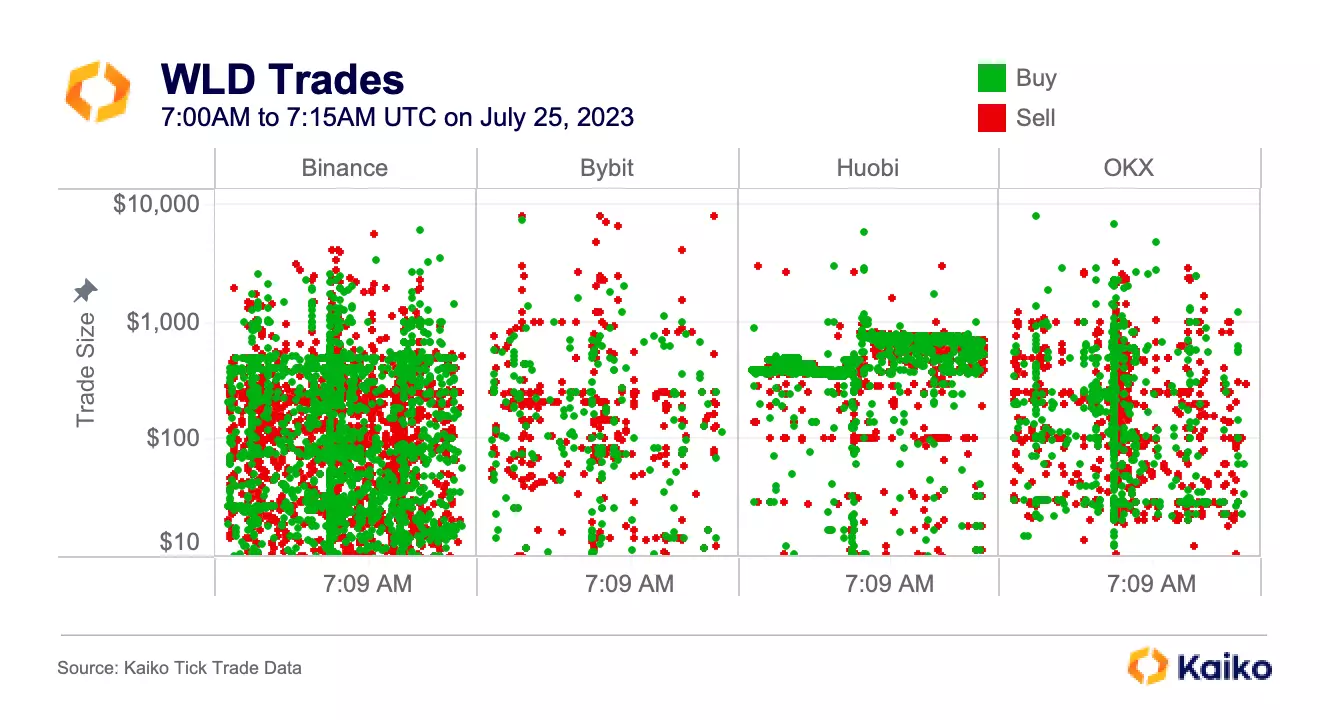

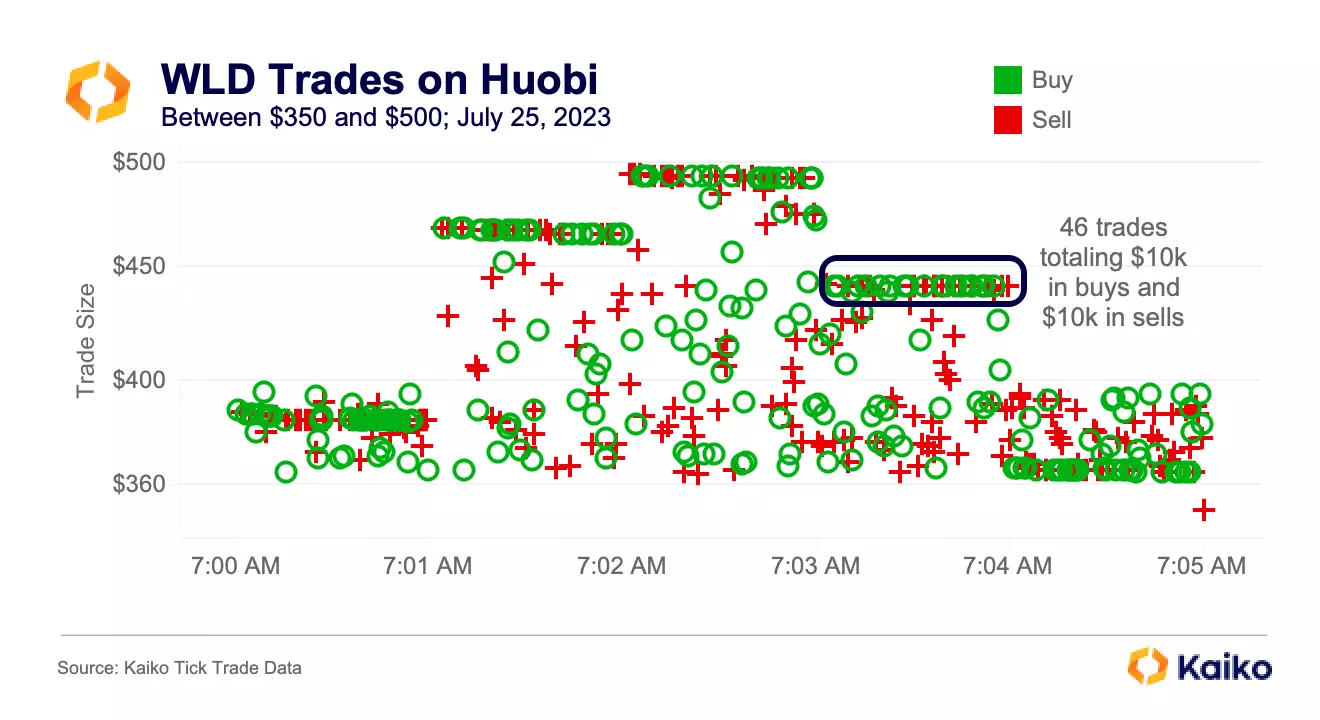

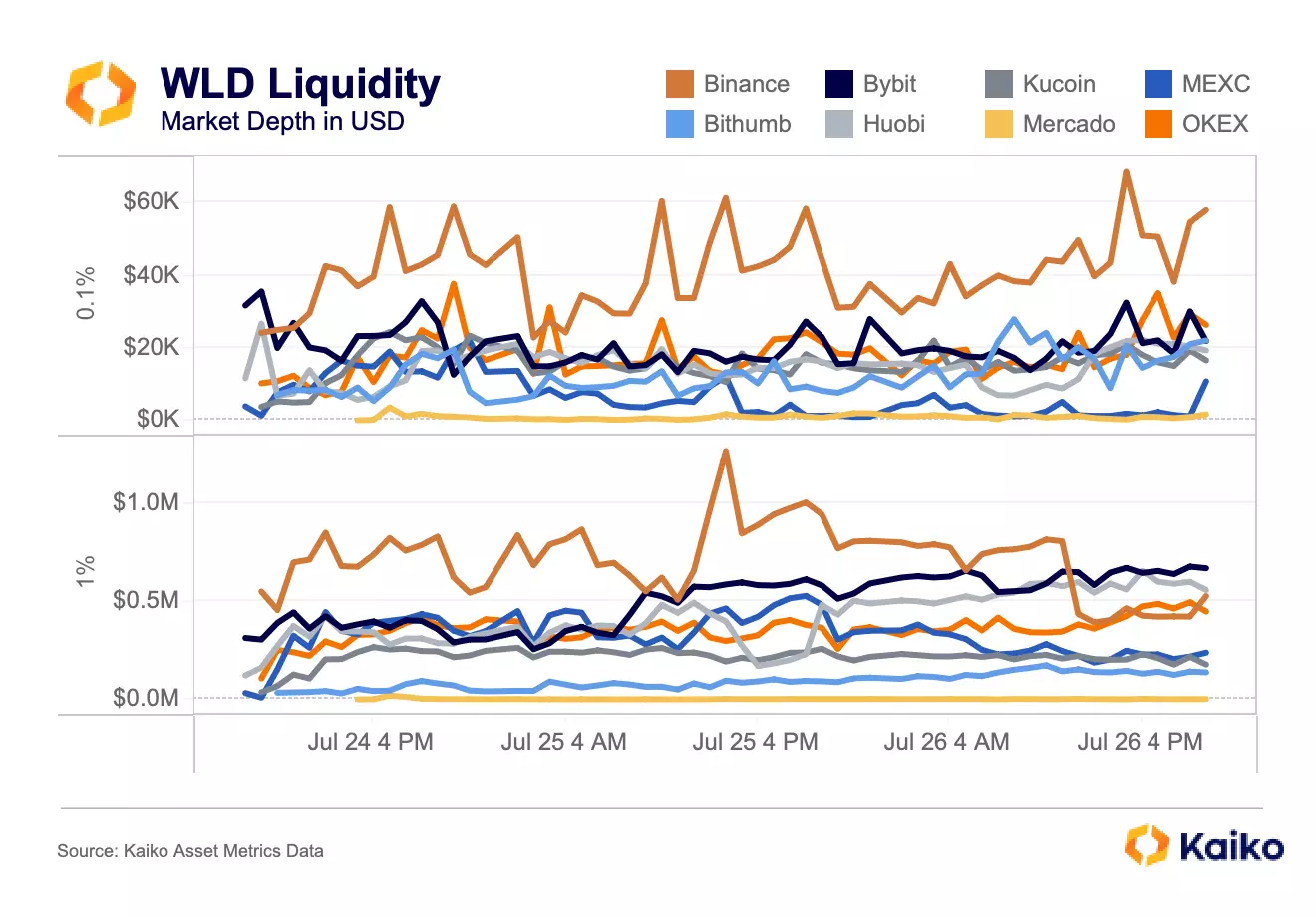

Worldcoin’s launch was one of the most unique and controversial in recent years. Much of the controversy stems from the understandable skittishness with Worldcoin’s goal (creating a global identity network) and sci-fi-like methods of achieving this goal (eyeball scans). This has been nicely summarized by the MIT Technology Review here. I’ll instead focus on why this launch was unique by analyzing tokenomics, trading, and liquidity.

More From Kaiko Research

![]()

CEX

25/07/2024 Deep Dive

What's Behind Turkey's Booming Crypto Market?Welcome to the Deep Dive! This week, we take a closer look at the rapidly growing Turkish crypto market. We’ll focus on the exchange landscape and evolving crypto regulation in Turkey.

Written by Dessislava Aubert![]()

Ethereum

22/07/2024 Data Debrief

Will the launch of spot ETH ETF be sell the news event?BTC surged above $67K following a massive global IT outage, Joe Biden ended his reelection bid on Sunday night, Indian exchange WazirX halted trading at it experienced a $230 million hack.

Written by The Kaiko Research Team![]()

ETF

19/07/2024 Deep Dive

BTC ETF 의 현물 시장 영향이번 주 리포트에서는 비트코인(BTC) ETF가 현물 BTC 시장 구조에 미친 영향을 분석하겠습니다. 특히 거래 활동과 유동성 측면에서 BTC ETF가 어떤 변화를 야기했는지 확인해 보겠습니다.

Written by Adam Morgan McCarthy![]()

Ethereum

15/07/2024 Data Debrief

ETH Spot Market Cools as Wait for ETF Launch IntensifiesU.S. inflation cooled further in June, bolstering the case for a September rate cut. BTC traded above $62K in the early hours of Monday, up nearly 11% over the past seven days. The SEC dropped its investigation into Paxos and BUSD on Thursday, while a voteto overturn President Biden’s veto of the SEC’s SAB 121 failed to reach the required majority in the House.

Written by The Kaiko Research Team