Now Available: Q2 2024 Crypto Market Report

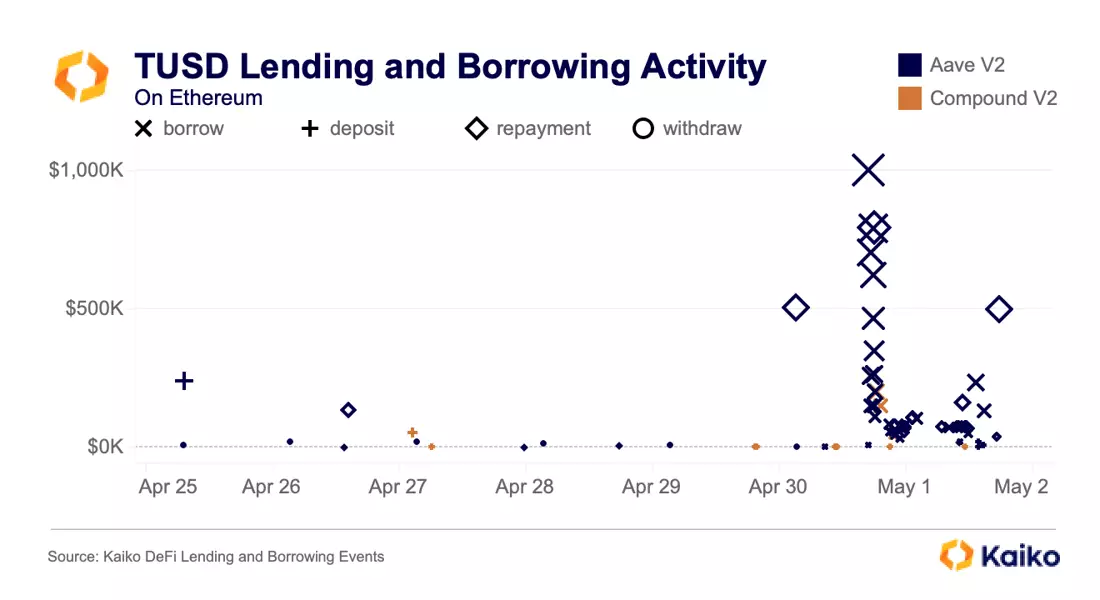

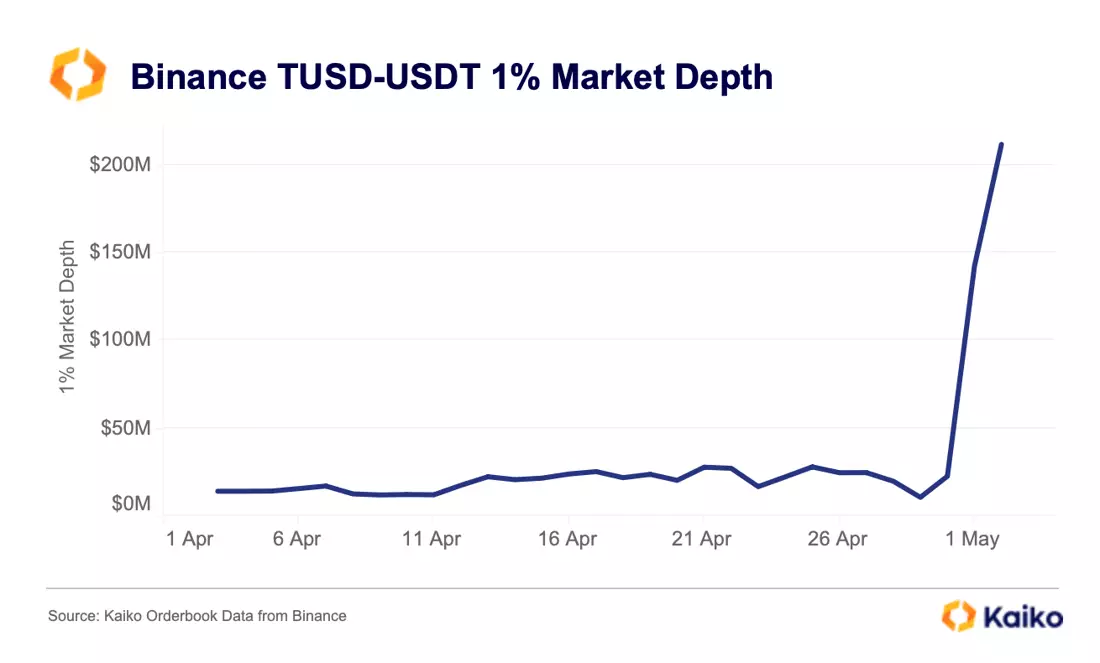

TUSD Depegs Amidst Heavy Borrowing

Written by The Kaiko Research Team

02/05/2023

Data Used in this Analysis

Derivatives Metrics

![]()

Metrics and analytics products tailored to the cryptocurrency derivatives market.

Liquidity Metrics

![]()

The most granular order book data in the industry optimized for quantitative analyis.

Trade Volume

![]()

Centralized exchange data sourced from the most liquid venues, covering all traded instruments.

More From Kaiko Research

![]()

CEX

25/07/2024 Deep Dive

What's Behind Turkey's Booming Crypto Market?Welcome to the Deep Dive! This week, we take a closer look at the rapidly growing Turkish crypto market. We’ll focus on the exchange landscape and evolving crypto regulation in Turkey.

Written by Dessislava Aubert![]()

Ethereum

22/07/2024 Data Debrief

Will the launch of spot ETH ETF be sell the news event?BTC surged above $67K following a massive global IT outage, Joe Biden ended his reelection bid on Sunday night, Indian exchange WazirX halted trading at it experienced a $230 million hack.

Written by The Kaiko Research Team![]()

ETF

19/07/2024 Deep Dive

BTC ETF 의 현물 시장 영향이번 주 리포트에서는 비트코인(BTC) ETF가 현물 BTC 시장 구조에 미친 영향을 분석하겠습니다. 특히 거래 활동과 유동성 측면에서 BTC ETF가 어떤 변화를 야기했는지 확인해 보겠습니다.

Written by Adam Morgan McCarthy![]()

Ethereum

15/07/2024 Data Debrief

ETH Spot Market Cools as Wait for ETF Launch IntensifiesU.S. inflation cooled further in June, bolstering the case for a September rate cut. BTC traded above $62K in the early hours of Monday, up nearly 11% over the past seven days. The SEC dropped its investigation into Paxos and BUSD on Thursday, while a voteto overturn President Biden’s veto of the SEC’s SAB 121 failed to reach the required majority in the House.

Written by The Kaiko Research Team