Kaiko's Q1 market report is now live!

Leveraging LSDs: The Next Era of Lending and Borrowing

Written by Riyad Carey

27/04/2023

Welcome to Deep Dive!

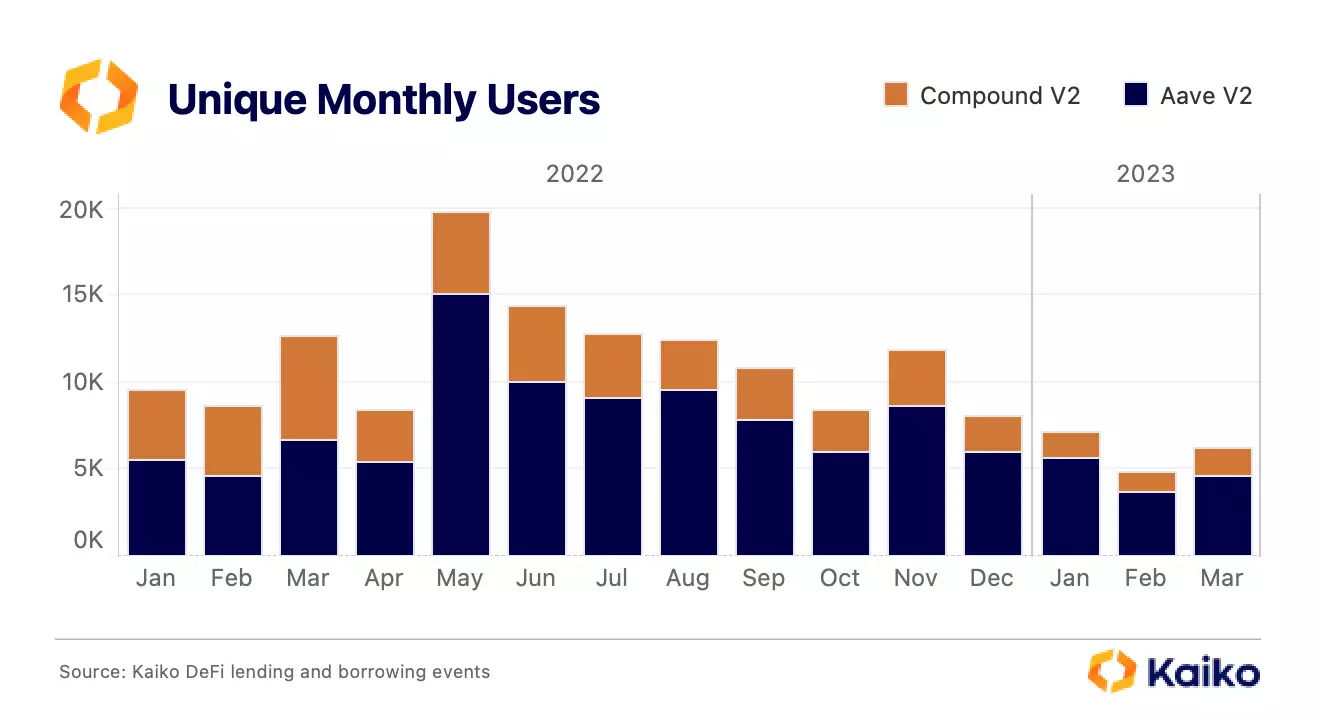

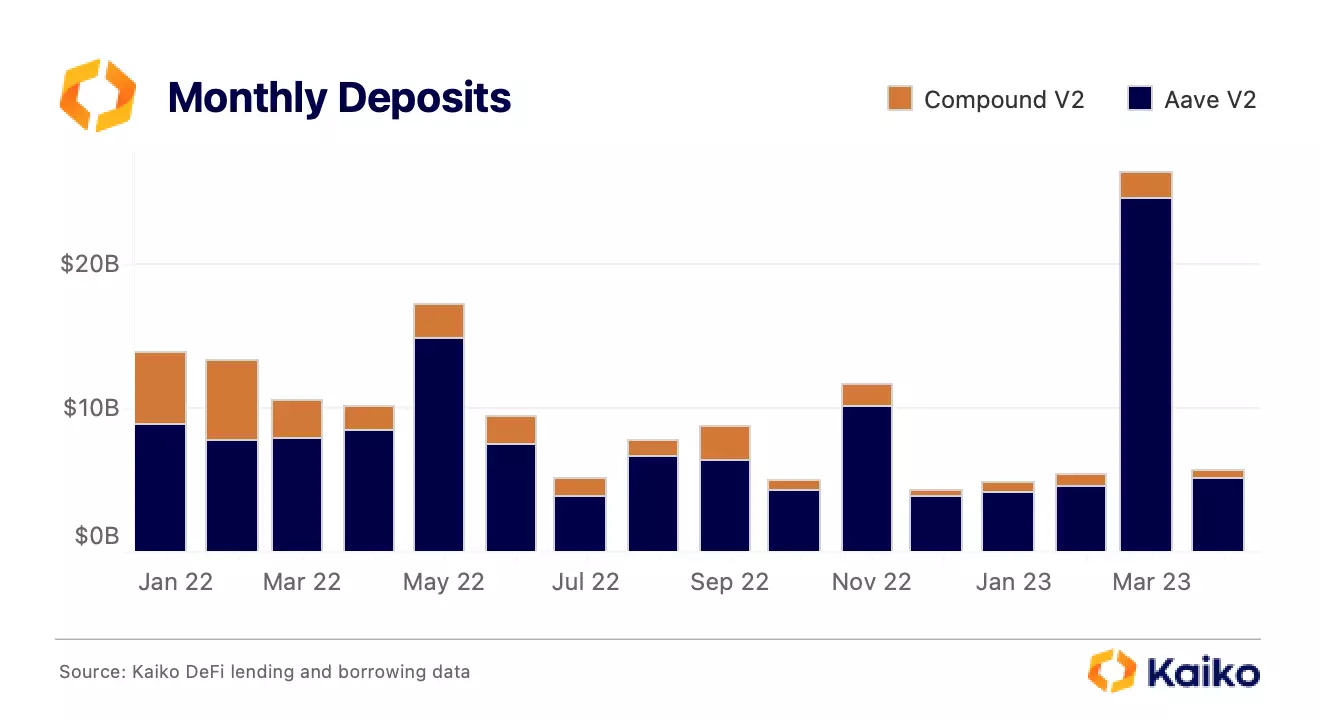

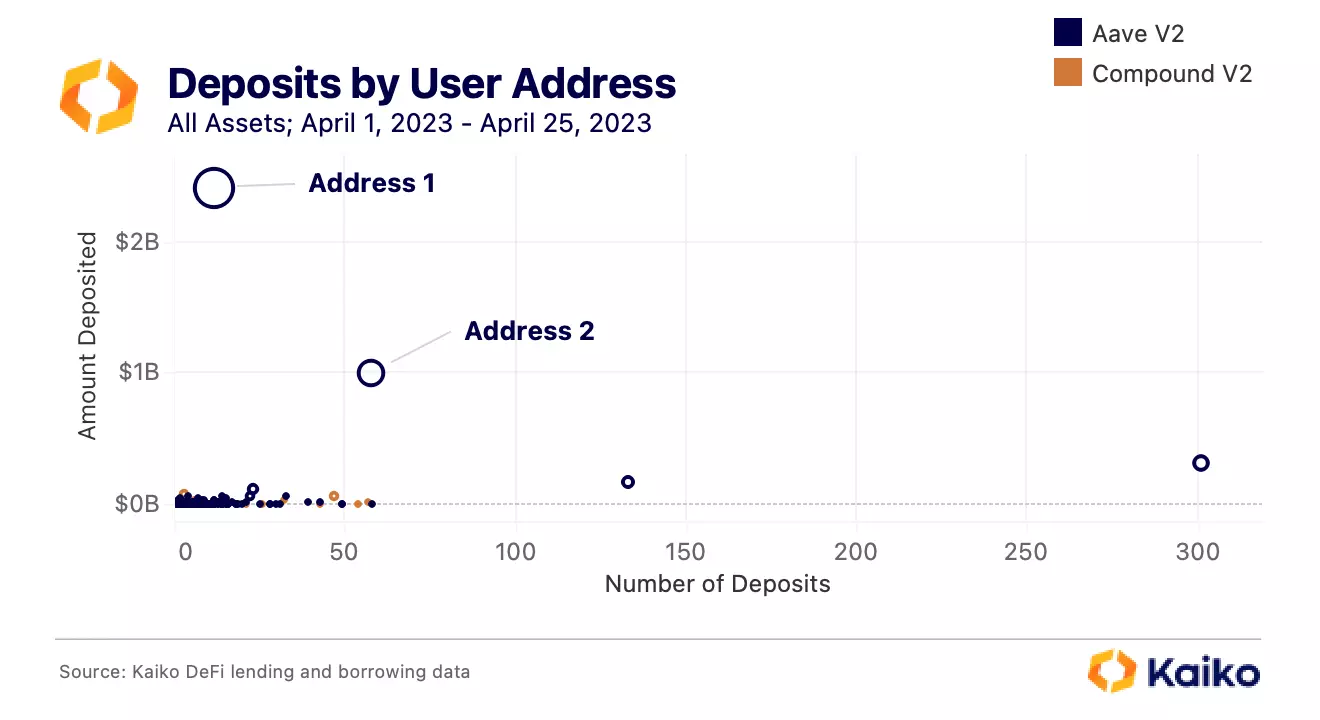

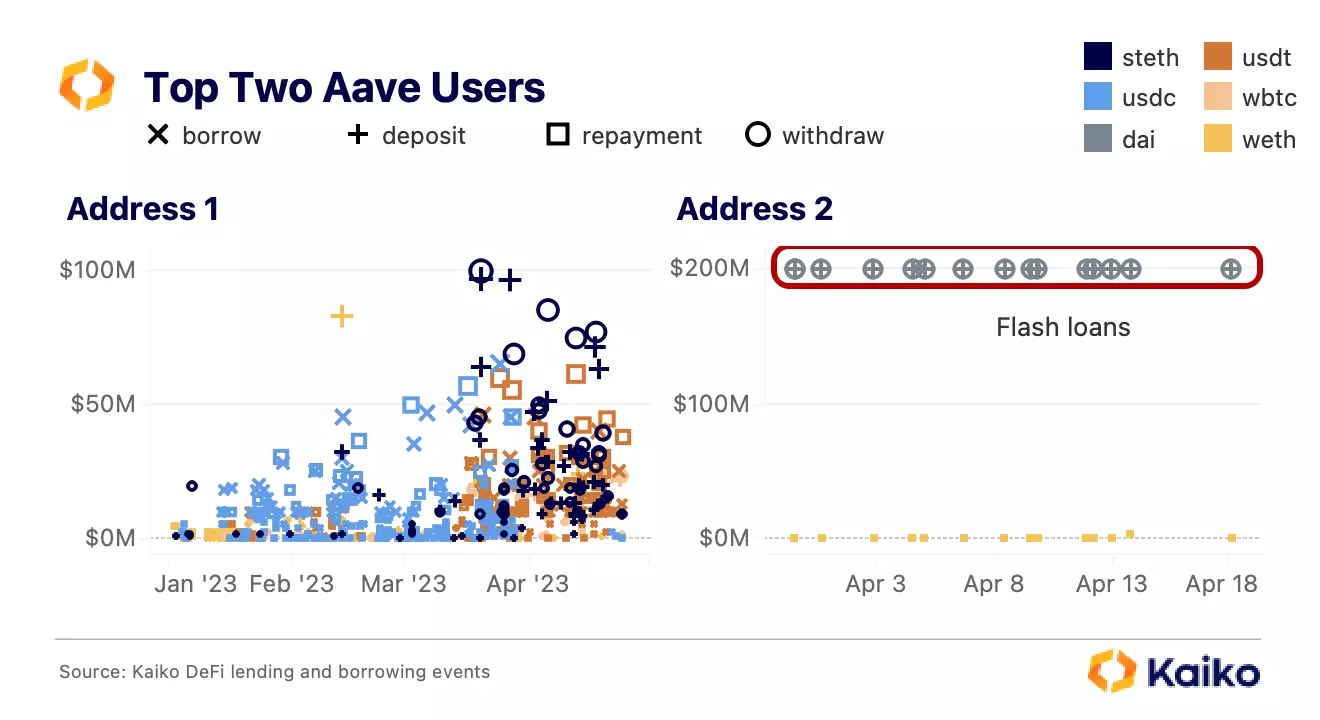

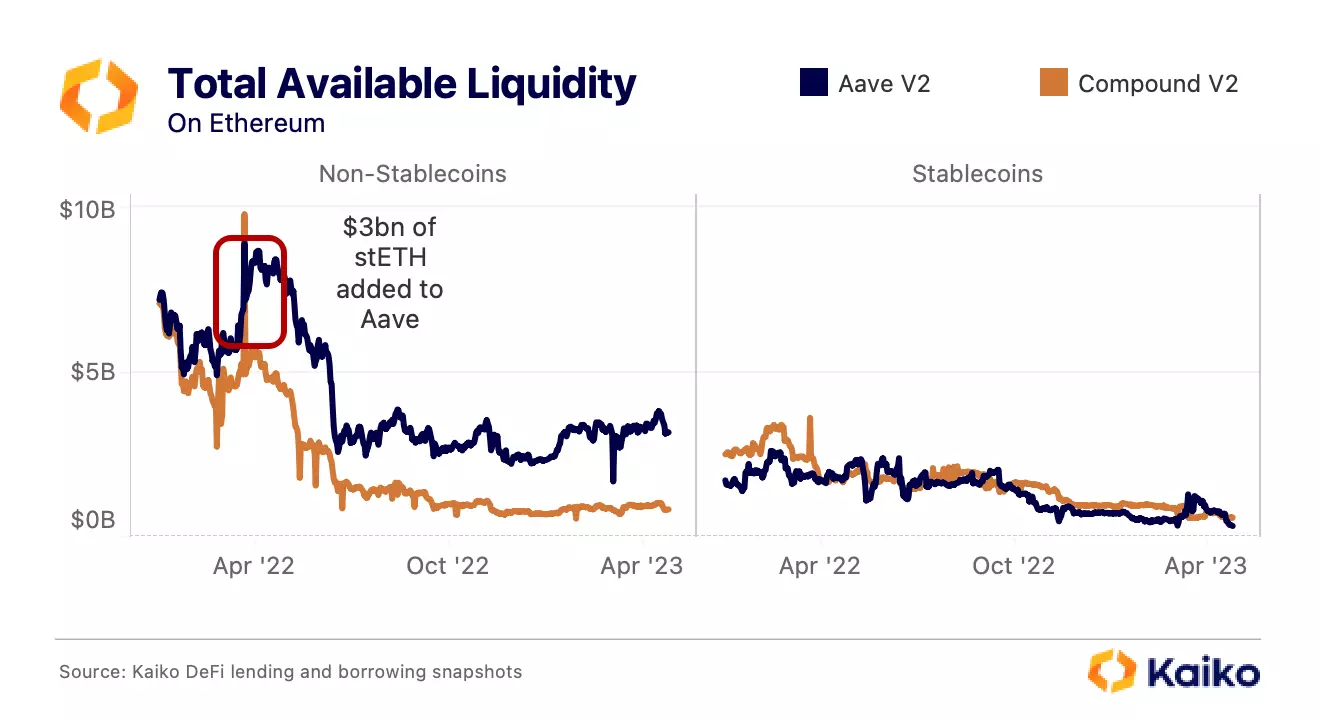

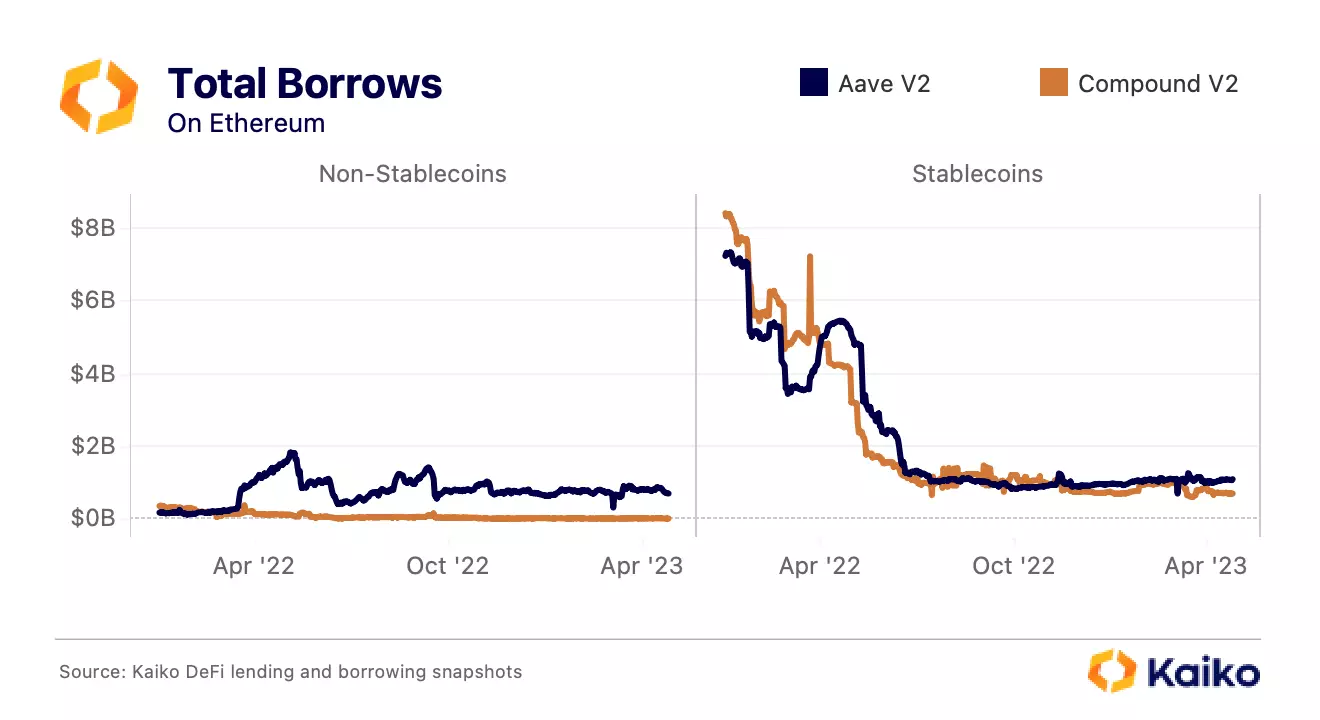

The best design often goes unnoticed. DeFi lending and borrowing stalwarts Aave and Compound have proven themselves to be great design: critical for day-to-day functioning but largely taken for granted. This becomes apparent when a competitor experiences an exploit, highlighting the reliability of Aave and Compound[1].

More From Kaiko Research

![]()

Bitcoin

25/04/2024 Deep Dive

Bitcoin's Fourth Halving: This Time is Different?This week we’ll provide an update on Bitcoin’s fourth halving, the impact its having on the market so far, and what to will drive demand in the coming months.

Written by Adam Morgan McCarthy![]()

Bitcoin

22/04/2024 Data Debrief

Bitcoin Halving Is HereWelcome to the Data Debrief! The much-anticipated fourth Bitcoin halving went live on April 20. While BTC ended the week flat, transaction fees experienced strong volatility following the launch of Runes, a protocol for issuing fungible tokens on Bitcoin.

Written by The Kaiko Research Team![]()

Asia

15/04/2024 Data Debrief

Crypto Fee War Heats Up in South KoreaWelcome to the Data Debrief! Last week, BTC fell in tandem with risk assets amid escalating geopolitical tensions. However, it regained ground early on Monday after Hong Kong reportedly approved spot BTC and ETH ETFs. In other news, the U.S. SEC issued a Wells notice to Uniswap Labs, and MarginFi experienced over $200 million in outflows as its founder exited.

Written by The Kaiko Research Team![]()

Bitcoin

08/04/2024 Data Debrief

All Eyes on the Bitcoin HalvingWelcome to the Data Debrief! BTC had a shaky start of the new quarter, closing last week flat before surging above $72k early Monday. In other news, DeFi protocol Ethena airdroped its ENA token, Ripple announced a stablecoin, and the Ethereum Foundation proposed to reduce ETH issuance.

Written by The Kaiko Research Team