Kaiko's Q1 market report is now live!

TriCrypto: Curve’s Ace in the Hole

Written by Riyad Carey

11/05/2023

Welcome to Deep Dive!

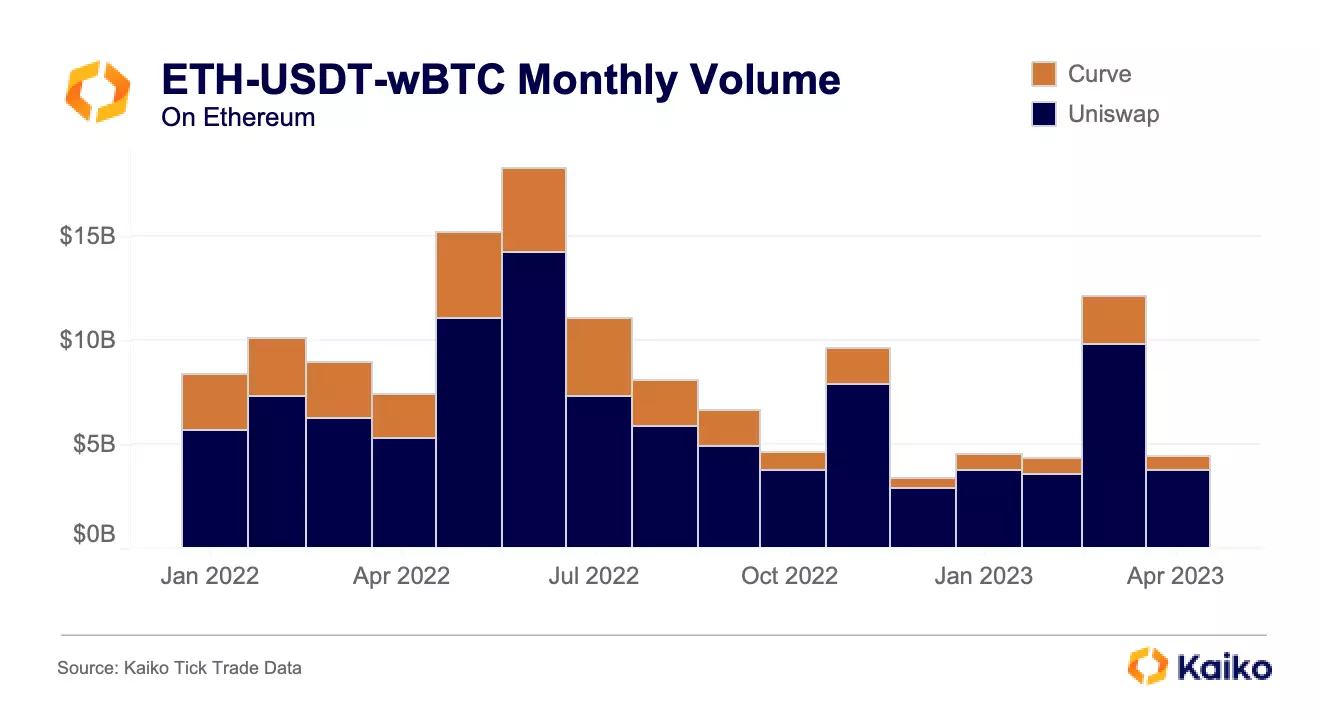

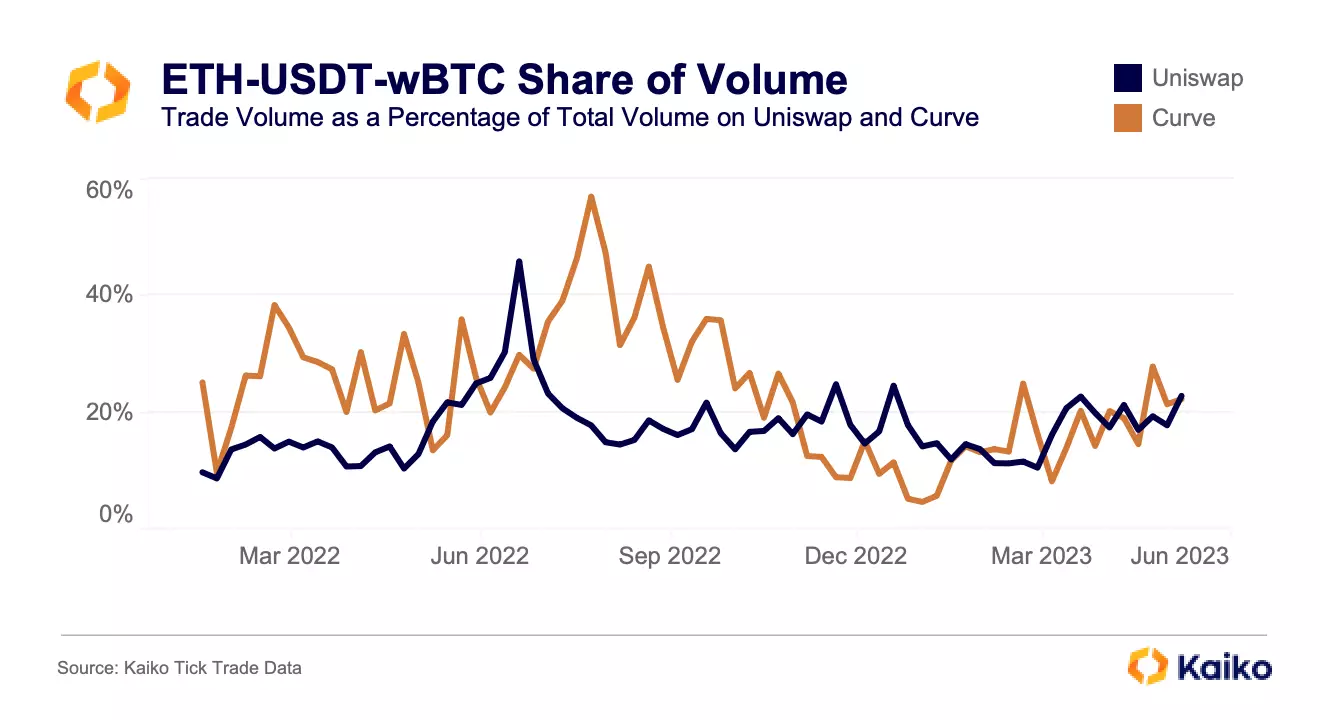

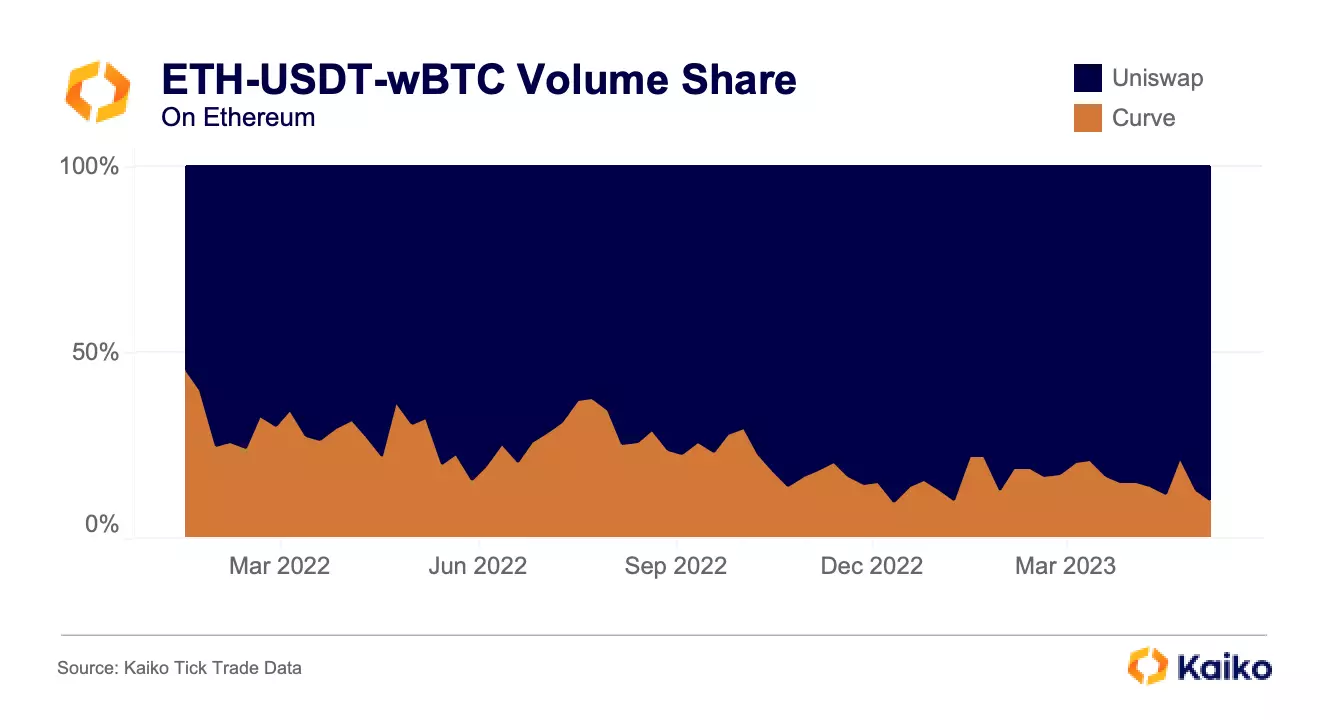

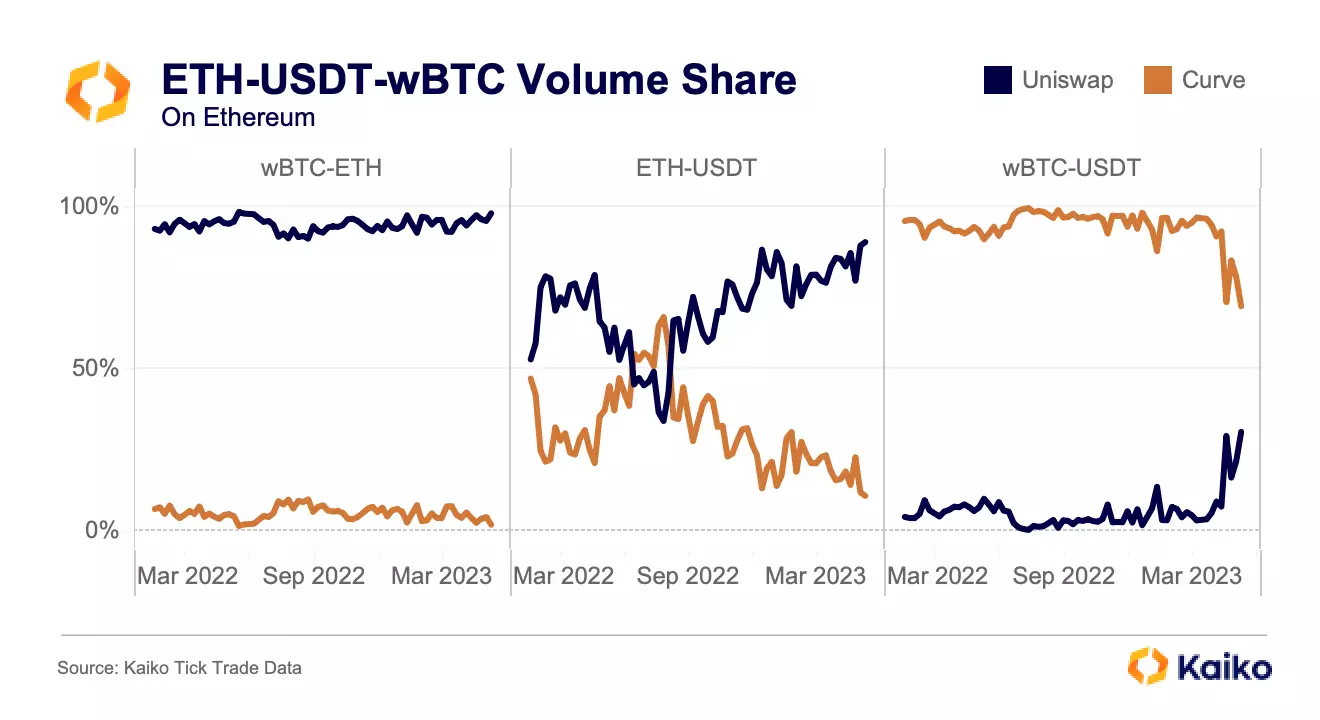

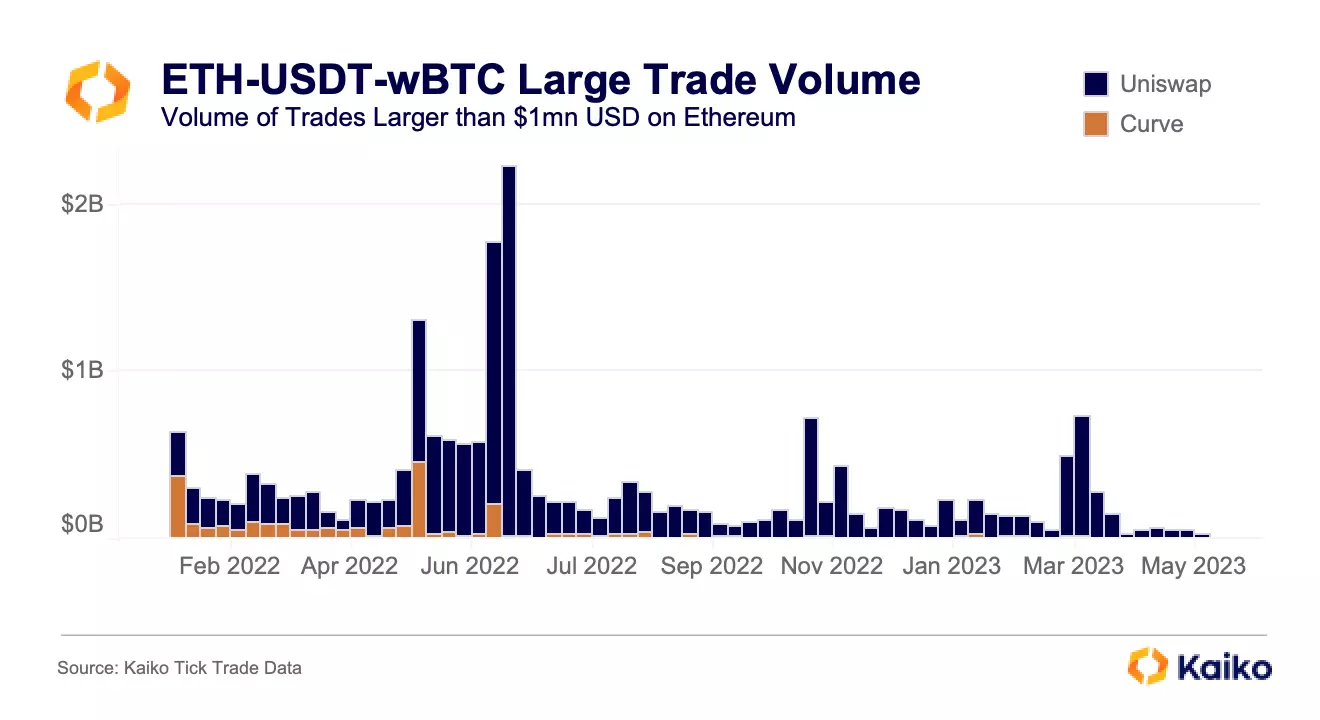

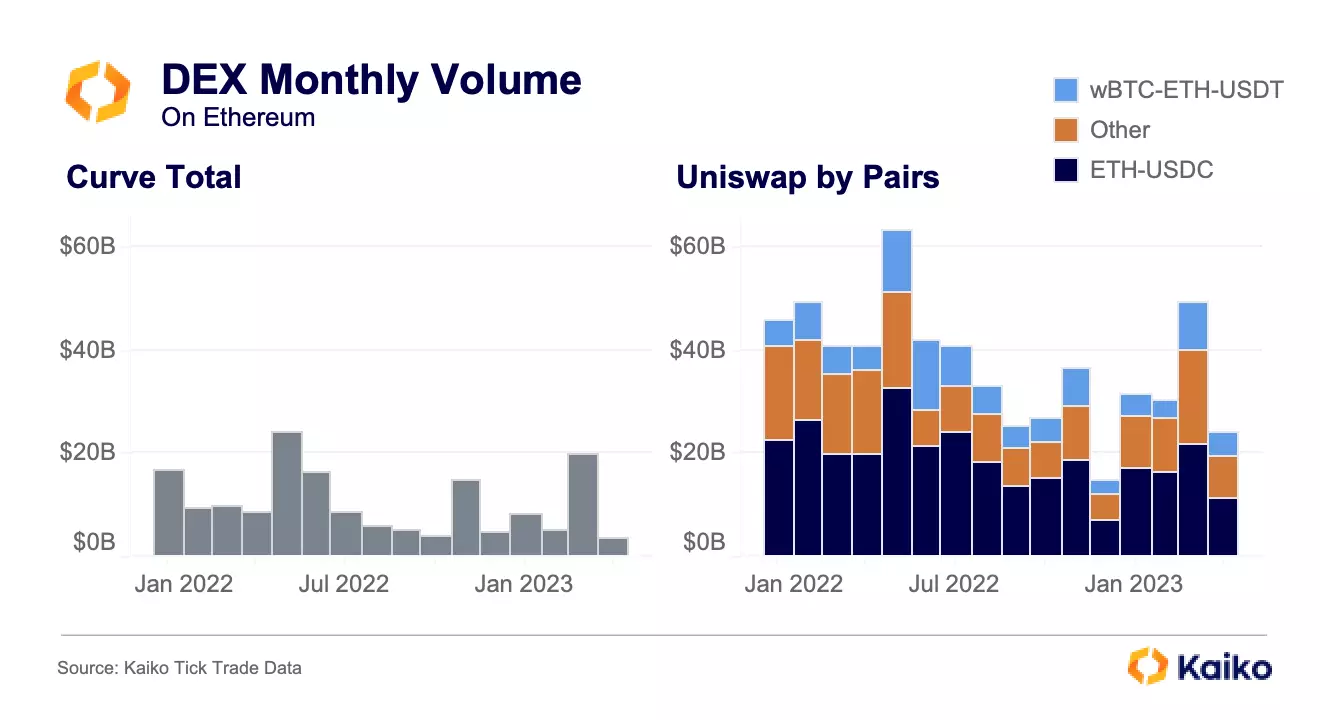

Curve recently made waves with the release of crvUSD, its new stablecoin. However, another under-the-radar development at Curve could cause an even more significant shift in the DeFi landscape: a new TriCrypto pool [1]. This pool contains three high-volume Ethereum assets—ETH, USDT, and wBTC—and could potentially challenge Uniswap’s market share. In this article, we’ll examine the current breakdown of market share and explore how the changes to TriCrypto could disrupt the status quo.

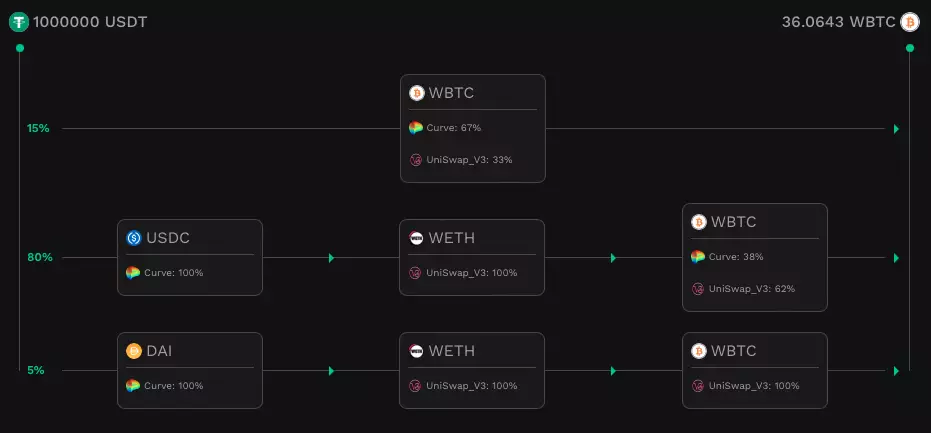

The release timing remains unclear, though tests have shown significant gas improvements and a replacement of USDT with USDC, two moves that could allow Curve to take a piece of Uniswap’s market share.

Curve hasn’t had a higher weekly volume of large trades since January 2022 and has been beaten $240mn to $1mn since the start of April.

Curve hasn’t had a higher weekly volume of large trades since January 2022 and has been beaten $240mn to $1mn since the start of April.

More From Kaiko Research

![]()

Asia

15/04/2024 Data Debrief

Crypto Fee War Heats Up in South KoreaWelcome to the Data Debrief! Last week, BTC fell in tandem with risk assets amid escalating geopolitical tensions. However, it regained ground early on Monday after Hong Kong reportedly approved spot BTC and ETH ETFs. In other news, the U.S. SEC issued a Wells notice to Uniswap Labs, and MarginFi experienced over $200 million in outflows as its founder exited.

Written by The Kaiko Research Team![]()

Bitcoin

08/04/2024 Data Debrief

All Eyes on the Bitcoin HalvingWelcome to the Data Debrief! BTC had a shaky start of the new quarter, closing last week flat before surging above $72k early Monday. In other news, DeFi protocol Ethena airdroped its ENA token, Ripple announced a stablecoin, and the Ethereum Foundation proposed to reduce ETH issuance.

Written by The Kaiko Research Team![]()

CEX

02/04/2024 Data Debrief

The Impact of the KuCoin ChargesBitcoin dropped 5% early Tuesday as the U.S. Dollar index climbed to four month highs. Meanwhile, SBF was sentenced to 25 years, three AI protocols announced plans to merge, and the London stock exchange decided to allow applications for crypto ETNs.

Written by The Kaiko Research Team![]()

Bitcoin

25/03/2024 Data Debrief

The Return of the Flash CrashBitcoin closed the week in the red, slipping to $67k, amid rising GBTC outflows. In other news, Blackrock unveiled its first tokenized fund on Ethereum, Genesis reached a $21mn settlement with the SEC, and the Ethereum Foundation is reportedly facing a probe by a regulator.

Written by The Kaiko Research Team